Fat Tailed Thoughts: Bank the Unbanked with Higher Overdraft Fees

Hey friends -

Big announcement - we're starting a podcast! I’ve thoroughly enjoyed the conversations sparked by these weekly letters and the podcast is an opportunity have even more.

New episodes will come out weekly following the letter. Expect 30 minutes of discussion and banter with my co-host and good friend Steven Dickens as we do our best to stay on topic with that week’s letter. You can check out the podcast here and subscribe on your choice of platform including Apple Podcasts and Spotify.

In this week's letter:

Overdraft fees - what are they, why Congress is up in arms, and how we’ve possibly already solved the problem

Sequoia shakes up venture capital, Vikings in the Americas, and more cocktail talk

Pear brandy is a game changer in the Saz Who? cocktail

Total read time: 11 minutes, 7 seconds.

No money, no problem!

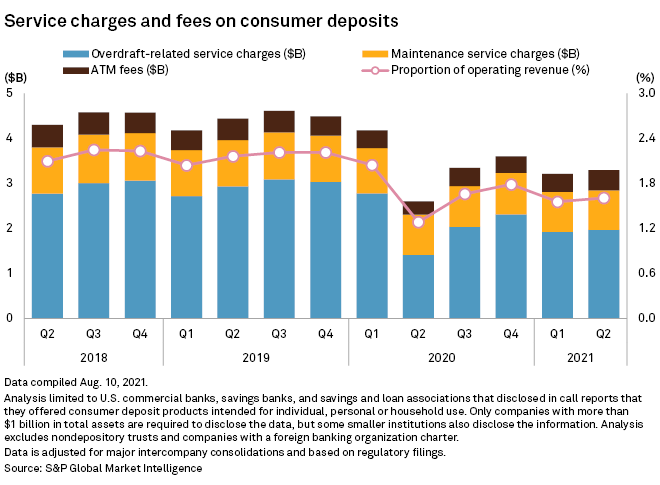

Overdraft fees. Banks charged almost $12 billion in overdrafts in 2019, a number that's only fallen due to pandemic-related relief. They still managed to charge billions throughout the pandemic.

You can imagine how that went over in the press and in congress. Back in May, a bunch of the big banks were hauled in for a hearing and the headlines have kept rolling ever since.

I find it all a bit confusing. If the issue were as simple as the headlines make it out to be - "overdraft fees are evil!" - I would’ve expected it to have been regulated out of existence a long time ago. The reality is much more interesting.

What are overdraft fees?

An overdraft is when you try to spend money out of your bank account that you don't have. You quite literally overdraw your bank account. This can take the form of a check that doesn't clear, an online bill payment that fails, an ATM withdrawal, or increasingly a debit card transaction. The last is worth emphasizing given the rapid growth in debit card transactions in the past 20 years.

Banks charge overdraft fees when you overdraw your account. There are four different types of fees lumped together as "overdraft fees" out of convenience, but are worthwhile to break out:

Overdraft coverage fee - a per overdraw incident fee if the bank approves a transaction that overdraws your account. If you make multiple overdraw attempts, you'll pay the fee multiple times.

Non-sufficient funds fee - a per overdraw incident fee if the bank does not approve a transaction that would overdraw your account. Like the overdraft fee, you can pay this multiple times.

Overdraft protection fee - a per overdraw incident fee if you opted into an overdraft protection service and attempt to overdraw your account. Typically this works by having a "back-up" bank savings account from which the money is transferred. Banks are not required to notify each time they approve an overdraft transfer.

Extended overdraft fee - if you fail to bring your account balance back above zero after an overdraft, you can incur additional charges until you do so.

Breaking out the fees highlights the weirdness of lumping them all together - they're not the same. Overdraft protection and non-sufficient fund fees are both purely transactional fees - they're incurred once during the transaction.

The overdraft coverage and extended overdraft fees together look a lot more like servicing costs on a loan. The bank agrees to lend you money short-term to cover the transaction. In return, you owe them an initial loan processing fee and then additional servicing fees until you pay it back.

It's a critical difference. Overdraft fees are not regulated as lending products today. Loans are subject to a whole host of restrictions, including how much the bank can charge, for good reason - in the wrong hands, they can be wildly predatory.

Consumer Protection

This appears to be an area ripe for consumer protection. Just take a look at the fee schedule for 16 of the largest US banks.

These fees generally aren't being charged against large transactions. The median transaction size that generates a fee other than a non-sufficient funds fee is $50. The overdraft protection is almost 25% of the transaction value and the overdraft fee is a whopping 70%!

Nor are the fees justified by bank customers who fail to pay back the bank. More than half of overdrafted accounts return to positive balances within three days and 76% do so within one week. Charged-off account balances - when the bank gives up on collecting repayment and typically closes the account - are only 14% of total overdraft fee revenue.

Overdraft protection usage is highly correlated with a person’s likelihood to make overdrafts that generate fees. Bank customers who opt into protection make 7 times more overdraft transactions that result in fees than those who do not.

Interestingly, "protection" seems to be better marketing than it is actual protection. Just 8% of account holders generate 74% of fees. When these super-overdrafters opt into protection, they typically incur an extra $347 in fees every year.

Who's paying these overdraft fees? Those least well situated to do so. They have average bank account balances of no more than $350, low credit scores, and limited access to credit on credit cards if any.

The structure of overdraft fees exacerbates the problems - it is the first lien on the bank account. As soon as the money hits your account, the bank is entitled to deduct the amount owed before you have any other rights to the money. Paycheck, child support, and social security payments are all treated equally - they go to paying back the bank first before you get what's left over.

Fee driven banks

While many of the big banks make headlines for the total fees charged, multiple truly bad banks have slipped beneath the public's radar. They're ignored because they're small - even the largest is less than 3% the size of JP Morgan.

For the top three offenders earning over 100% of overdraft fees as a percent of profit, this means that they net lost money on all of their other operations and overdraft fees keep them afloat. Beyond this being abusive to consumers, this is a frankly astonishing oversight by regulators charged with protecting safety and soundness of banking operations. How banks that are entirely reliant on fees charged to people who run out of money meet a "safe and sound" threshold is beyond me.

Legislators to the rescue

Congress and regulators have taken notice. Before 2010, banks could auto-opt-in customers to overdraft protection without notification. Under Regulation E, they're now required to disclose the fees in advance and customers have to opt-in for protection.

Much of the data cited here comes from a series of studies conducted by the Consumer Financial Protection Bureau (CFPB), a regulatory agency created by the Dodd-Frank Act responsible for consumer protection. The 2010 opt-in requirement created a "natural experiment" of how behavior and fees could change in response to legislative action.

While a good start, even this data is woefully incomplete. Only banks with assets greater than $10 billion are required to report to the CFPB. Credit unions and banks with assets less than $1 billion aren't required to report overdraft fee revenue at all. Given that the 5 of the top 6 "overdraft fee banks" highlighted in the diagram above have assets less than $3 billion, it seems probable that there are more abusive banks simply staying out of the limelight.

Not content with the progress made to date, Democratic congresspeople have made multiple attempts to pass new legislation that would curtail overdraft fees. In addition to strengthening disclosure requirements, the proposed legislation includes three key changes:

No more than one overdraft fee per month and six per year OR a complete prohibition on overdraft cover,

No non-sufficient funds fees for debit card or ATM transactions, and

Banks must process transactions in a manner that limits fees.

A modified version of the "processing transactions" requirement is already live in New York state. It prevents banks from choosing to process a large transaction first that drives an account negative and then collect fees for all subsequent transactions against the negative account. Instead, banks can either process the transactions in the order they come in or in a manner that limits the fees.

Despite the headlines, none of the proposed federal legislation is on track to pass into law anytime soon. The bills have not been discussed widely in committees and they have few co-sponsors. Skopos Labs puts the odds at less than 3%. But it turns out that might not actually be a bad thing. The cure may be worse than the disease.

A Worse Alternative

The purpose of the proposed legislation is to protect the vulnerable. From the preamble to both the House of Representatives and Senate bills:

Such abusive practices in connection with overdraft coverage fees have deprived consumers of meaningful options and placed significant financial burdens on low- and moderate-income consumers.

That's noble. Almost 25% of low-income households in the US are unbanked and the potential for overdraft fees is a likely contributing cause. But that statement's not necessarily transitive. It doesn't actually answer the key question: can limiting overdraft fees promote financial inclusion?

A recent working paper looks into exactly that question. It seems Congress and the regulators ignored another "natural experiment" from 2001 when state-imposed overdraft fee limits were relaxed for nationally chartered banks. We can look at how financial inclusion changed for those banks who could charge more fees and use the banks that couldn't as the control group.

The paper uncovers three key findings:

Banks allowed to increase their fees did so by an average of $2, about a 10% increase. But, they also were more willing to cover overdrafts. In the early 2000s, about 10% of banks still refused to process transactions that would result in overdrafts. As they increased fees, more banks offered overdraft services.

The newly available overdraft had tangible and immediate benefits to bank customers. Banks bounced 10% fewer checks, meaning that transactions that would previously have failed due to lack of funds were processed anyways with the bank fronting the money.

These changes resulted in a 4% increase in checking account ownership by low-income households, a 10% increase in the probability that a low-income household has a bank account at all.

These findings are unidirectional - freeing banks to charge more overdraft fees resulted in more low-income households getting bank accounts. The data even demonstrates that not only did they open more bank accounts, but they also held onto those accounts at a higher rate than before fees increased. It appears that at least for the early 2000s period studied, even the effects of any shortcomings in bank disclosures regarding fees were overwhelmed by the value offered by making overdraft services more widely available.

Maybe the spectacle is the cure

At this point, we could go in several different directions. We could advocate for new legislation by challenging the study that demonstrates higher overdraft fees leading to increased access to banking for low-income families - the study only included four US states, we have no insights into the effects by protected classes, and the period studied was before the modern digital banking experience and rapid growth of debit card transactions. By contrast, we could instead argue that the proposed legislation is clearly misguided based on the results from a compelling natural experiment and related research into the effects of price ceilings and abusive lending rate limits.

We're going in a third direction - all the noise and hubbub from Congress and the media is exactly what was needed.

The attention has made overdraft fees a meaningful factor for consumers. New solutions - without any legislation - have rapidly emerged to meet consumer demand. Startups like Brigit offer a $10 per month membership where they will advance up to $250 at zero interest to cover any unforeseen overdrafts so you avoid any additional fees. Earnin will advance you up to $500 also at zero interest ahead of your paycheck showing up and the only fees are whatever "tips" you choose to send the company for offering the service.

Banks are now starting to compete as well. Ally, Axos, Discover, and many others eliminated all overdraft fees. Huntington instituted a 24-hour no-fee grace period, no fees on overdrafts up to $50, and automatic qualification for personal lines of credit up to $1,000.

This is what competition looks like. These startups and banks are winning customers by offering better services at cheaper prices. Congress and the regulators did their part - they made an enormous amount of noise and put on a clown show built for Tweetable headlines of big bank CEOs defending overdraft fees. The news machine ate it up and brought it to the forefront of consumers' minds. Now the market is doing its part - facilitating real competition where the customer is the ultimate winner.

My hope is that this continues in earnest. I'm not excusing First Convenience Bank and its peers rampantly fleecing consumers under the guise of offering banking services. They're a prime example of where regulators can step in to protect consumers and create a healthier system. I'm focused on the extraordinary new services available to you and me.

The headlines have forced our banks to compete to allow us to spend money we don't yet have in our accounts - and increasingly do so for free - rather than reject transactions outright. Internet bills, utility bills, and all varieties of other recurring payments are now far less likely to be bounced, meaning no more interruptions in service just because of an accidentally missed payment. That's real, tangible value that will keep getting better if only we allow competition to continue to play out.

Cocktail Talk

Sequoia, a venture capital firm, is taking a leap into the unknown. They've faced recent and rapidly increasing competition. Hedge funds, private equity, family offices, and others have all started making direct investments in startups, bypassing the venture capitalists, to the tune of many billions of dollars. Sequoia has responded by becoming a Registered Investment Advisor and fundamentally retooling how they allocate capital. (Twitter)

A new paper published in Nature dates Viking settlements in the Americas to 1021 AD. Really cool science. From the article: "Anatomical characteristics such as different numbers of growth rings... show that wood items... comprise at least two different species, specifically fir, possibly balsam fir (Abies cf. balsamea), and juniper/thuja... The determining factors were their location within the Norse deposit and the fact that they had all been modified by metal tools, evident from their characteristically clean, low angle-in cuts. Such implements were not manufactured by the Indigenous inhabitants of the area at the time." (Nature)

Explosive material from Google's antitrust filing. Highlights (lowlights?) include an illegal agreement with Facebook codenamed "Jedi Blue" which includes how they'll cover up if anyone finds out and a dedicated "gTrade" team responsible for manipulating ad markets. (Twitter)

In a farewell to Luddites, Tokyo is upgrading from 1900s floppy disk technology into the 21st century just two years after the US nuclear forces. I highly recommend checking out C4ISRNET's pictures of the 1970s tech that powered the world's premier nuclear force until 2019. (Nikkei, C4ISRNET)

Your Weekly Cocktail

A pearfectly (sorry) rethought classic courtesy of Death & Co.

Saz Who?

1.5oz Bully Boy Rum Cooperative #2

0.5oz Clear Creek Pear Brandy

2 dashes Absinthe

1 tsp Coconut Sugar Syrup

4 dashes Peychaud’s Bitters

1 dash Angostura Bitters

Lemon peel for spritz

Pour all of the ingredients (except the peel) into a mixing glass. Add ice until it comes up over the top of the liquid. Stir for 20 seconds (~50 stirs) until the outside of the glass is frosted. Strain the cocktail into a rocks glass, no ice. Squeeze the lemon peel over the top of the glass to express the oils and discard. Enjoy!

This is a modified version of the original created by Brian Miller at Death & Company in 2009. While this cocktail takes inspiration from the Sazerac, it’s way off the beaten path. I’ve wanted a cocktail that incorporates the Clear Creek Pear Brandy for some time, but I’ve been unable to do it justice myself. It takes 20 pounds of pears to make a single bottle of Clear Creek and the result is spectacular. It is somehow more pear-flavored than an actual pear and brings that deep-in-the-chest warmth so distinctive of an eau de vie. Here it plays brilliantly with a lighter rum and more than holds its own against the aggressive mix of absinthe and bitters. This one’s going to keep being a learning experience for me as I discover more ways of pairing it. In the meantime, in a glass in front of the fire will do just fine.

Cheers,

Jared