Fat Tailed Thoughts: In Defense of Stupidity

Hey friends -

Welcome to everyone who signed up this past week! Each week we explore 1-2 topics, often centered on growth and change. You'll find topics ranging from business and economics to biology and the natural world. And a cocktail, because why not? Suggestions for future topics - and drinks - much appreciated!

In this week's letter:

In defense of stupidity: why letting hedge funds lose spectacular sums of money is good for the system

Facts, figures, and links to keep you thinking over a drink

A drink to think it over

Total read time: 15 minutes, 53 seconds.

The Gooey Kablooie

Back in March, a then mostly unknown family office by the name of Archegos Capital Management blew up. Blew up, in this case, means it - we're talking $20 billion to $0 in ten days. In the days that followed, we saw the as-expected calls for increased regulation.

For those of us that weren't following the minutia of how this continued to evolve, yours truly included, it appeared that the saga was over. Rich guy blows up, the world goes on. But no. July 29th saw a flurry of proposed bills approved by the House Financial Services Committee with two aimed at "solving" Archegos-type problems.

That begs two questions:

Was Archegos even a problem?

Do the proposed regulations pass the "first, do no harm" test?

To answer, let's first take a look at what happened with Archegos and then look at similar examples of other firms blowing up to see if we can find a trend. We'll use that understanding to evaluate the proposed regulations.

How to lose $20 billion in ten days

Even among the annals of blown-up funds, $20 billion to bankruptcy in two days is an accomplishment. Like most of the firms we'll explore, Archegos employed a tremendous amount of leverage. Leverage is using borrowed money to invest. Leverage works both ways - it enhances returns and losses - a fact forgotten at investors' peril.

Let's take a simple example to understand the effects of leverage. Sally only has $50 but wants to buy $100 of stocks. Billy loans Sally $50 so she can buy the $100 of stocks and in return Sally pays Billy an interest rate. We say Sally is leveraged 1-to-1 because she has $50 of debt and $50 of cash. If the price of the stocks goes up by 50% after Sally purchases, she'll make $50 after paying back the loan and whatever she owes in interest. But if the price of the stocks goes down by 50%, she loses the entire $50 she owns and still has to pay back the $50 loan. Leverage is a double-edged sword.

Back to Archegos, a family office that was run by Bill Hwang. Family offices are what they sound like - firms that just manage the money of a family. Hwang had a storied-then-infamous career throughout the early 2000s as a hedge fund manager. After producing spectacular returns for investors in a seven-year run from 2001-2008, Hwang's fund lost 23% of its value in 2008. The fund was then criminally convicted of wire fraud in 2012 and settled with the SEC (the main regulator for the firm) on insider trading charges for $44 million, while Hwang himself was banned from trading in Hong Kong for four years starting in 2014. All of this information is and was publicly available.

Despite losing lots of investors' money and running afoul of the law, Hwang nonetheless had plenty of money from his early years. In 2013, he launched Archegos as a family office responsible for managing his $200 million.

Leverage cuts both ways

By early 2021, Archegos had turned the original $200 million into about $10 billion. As would later become apparent, much of the return was likely attributable to Hwang taking on extraordinary leverage but forgetting that it cuts both ways.

In the aftermath, it appears that Archegos was leveraged between 5-to-1 and 8-to-1 using money loaned to the family office by banks. At the upper end of this range, that means his $10 billion allowed him to purchase almost $100 billion worth of stocks and other financial assets. Such leverage can, in theory, be used without taking on as much risk as would otherwise be expected. The term hedge in hedge funds comes from such an approach. If an investor sets up a trade such that they make money when a stock goes up or down, we say they have hedged some of the risks. In practice, effective hedges are difficult to design and risks of poorly designed hedges increase with leverage. Archegos didn't even try to properly hedge.

Hwang piled tens of billions of borrowed dollars into just a couple of publicly traded companies including Viacom. At one point, Archegos likely owned over 30% of Viacom that almost entirely bought with borrowed money. Like with saw with Billy and Sally, a small drop in the price of Viacom could cause big problems for Archegos.

In two days, the price of Viacom dropped over 30% and Archegos couldn't pay back the banks. This is where the story gets really interesting.

Pennywise and pound foolish

All of this leverage went unreported before Archegos blew up. What Hwang did was engage multiple banks, each of whom only lent him some of the money. He borrowed from Credit Suisse, Morgan Stanley, Goldman Sachs, and others. At each firm, he set up a similar financial structure called a total return swap. The swap meant that the banks purchased and held the stocks on behalf of Archegos. If the price of stocks went up, the banks paid Archegos. If the price went down, Archegos had to put up more cash as margin (reminder from last week: margin is the cash that the bank will seize if stuff goes wrong).

Why would the banks offer such a deal to Archegos? Fees. The banks got paid big fees for writing the total return swap in the first place and then got an ongoing interest rate fee for the life of the swap.

Had each of the banks known that Hwang was doing the same deal with multiple other banks, they probably would've declined to lend him more money. His previous shenanigans should be a red flag for anyone doing business with him, as it was for JP Morgan who declined to take him on as a client. No one forced the banks to do business with Hwang or to forego their normal due diligence.

Yelling fire in a crowded theater

As Viacom's price trended south and it became clear that Archegos couldn't pay back its loans, the banks that lent the firm money finally asked the questions they should've at the beginning. Now knowledgeable about the full extent of Archegos's leverage, the banks realized what was coming and moved to cover their losses as quickly as possible by selling the Viacom stock.

Remember how this whole thing played out - a bunch of banks owned over 30% of Viacom on behalf of Archegos but collectively had lent the firm something like 8x the amount of money that Archegos had in cash. The fastest way to dump Archegos as a client and get cash to pay off the debt Archegos owed was to sell the shares of Viacom. The banks knew that with such a large position of Viacom stock, as soon as they started selling, the price of Viacom would crash. This caused a race for the exits by all of the banks, with winners and losers based on who made it out the door first.

The most recent count of losses is as follows:

Goldman Sachs - $0 (guess who was first to sell the shares?)

Deutsche Bank - $0 (guess who also sold super early?)

Mitsubishi Financial - $300 million

UBS - $861 million

Morgan Stanley - $911 million

Nomura - $2 billion

Credit Suisse - $5.5 billion

Almost $10 billion in losses, almost all in under a week.

Lessons from Archegos

What are the lessons to be learned here?

Banks sometimes take on risks that can lead to huge losses. We require banks to hold capital against trades like total return swaps in case something bad happens.

Sometimes risks interact in unpredictable ways that lead to much larger losses. We also require banks to hold additional capital beyond the amounts held on a trade-by-trade basis because we can't predict everything.

The banks didn't know how much leverage Archegos had in aggregate. Each bank has an underwriting department that has to approve all counterparties like Archegos. The banks also have risk departments that re-evaluate risk at multiple levels in the bank. There was no information here that the banks couldn't have figured out, they just didn't bother to or ignored it if they knew.

The banks’ share prices crashed and shareholders took big losses when it was announced that the banks lost money. That's exactly how the system is supposed to work.

All of these banks are still in business. No regulators needed to step in and no one needed to be bailed out. The capital protections we put in place worked as intended. Such an event is a good opportunity to review the regulations we have, but by all accounts, the existing regulations were a resounding success.

Archegos over-borrowed, the banks over-lent, they both took massive losses, and the world kept moving forward. That's exactly how this system is supposed to work.

History never repeats itself, but it does often rhyme

Maybe we got lucky with Archegos and the industry nonetheless needs new regulations to protect against the next bigger, messier Archegos. We have no shortage of firms that overleveraged and blew up, and we can probably glean some insights by looking at them. We'll widen our lens from just family offices to include hedge funds to find some truly remarkable stories.

Family offices and hedge funds have a key difference - a family offices manages a family's money whereas a hedge fund manages other people's money. Hedge fund managers typically get paid a fee for managing the money and a performance fee for making more money. As both fees increase with the amount of money they manage, hedge fund managers can be highly incentivized to grow the amount of money they manage even if they are taking on huge risks of losing money while doing so. By contrast, because family offices only manage their own money, they bear the full cost of losses. This means that even in the best of scenarios, a hedge fund typically is incentivized to take on more risk than a family office.

It's this risk-taking dynamic that makes hedge funds a rich source of stories about those who overleveraged and blew up.

Long Term Capital Management

No exploration of hedge fund blow-ups is complete without Long Term Capital Management (LTCM). From the $1 billion launch in 1994 until it’s spectacular failure, the hedge fund was generally well regarded in the industry. The fund grew to almost $5 billion by 1998, helped in part by the renown of counting not one but two Nobel Prize winners as members of the board of directors.

It's not easy to summarize the multiple different investment strategies LTCM pursued. What is easy to summarize is the leverage - 25-to-1 - totaling over $125 billion in borrowing. The firm's premise was that with sophisticated financial models it could effectively manage the risk of losing money such that a 25-to-1 leverage ratio wasn't as risky as it seemed. It worked well until it didn't.

Over the summer of 1998, the strategy failed and a trickle of losses became a flood. In August, the firm lost $1.8 billion and then another $1.9 billion in the first three weeks of September. By the last week in September, the firm had just $400 million in assets left against a remaining $100 billion in debt.

To avert disaster, the Federal Reserve Bank of New York hastily arranged a bailout, not from the taxpayers but from the banks with whom LTCM did business. All of the major firms participated except for Bear Sterns, a decision that would come back to bite them when they ran into trouble in 2008.

The eventual $4.6 billion in losses were borne entirely by LTCM, its investors, and the banks with whom they did business. The Fed's role, while important, was simply to coordinate the industry to collaborate on the bailout. A sudden and spectacular blow-up, but the impact was limited just to those involved in the hedge fund.

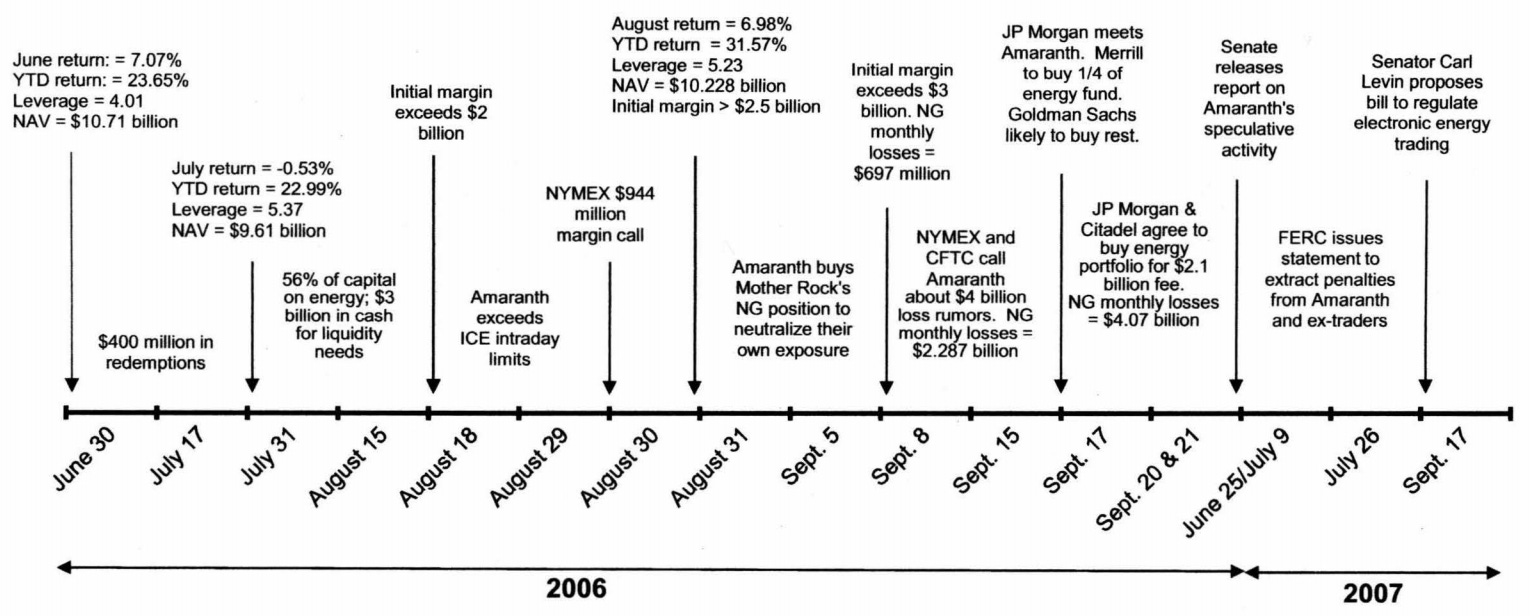

Amaranth

Another blow-up, another story about leverage. Amaranth was founded in 2000 and pursued a wide variety of investment strategies to great success. By 2006, the firm grew to be entrusted with over $9 billion of investor money. Between July 1 and September 21 of that year, the hedge fund spectacularly blew up.

Throughout 2005 and 2006, Amaranth bought billions of dollars of natural gas futures. A futures contract is a deal in which two parties agree now to exchange an agreed quantity of a good at an agreed future date where the price will fluctuate between now and the future date. Parties to futures contracts have to put up margin (cash) to limit the fallout if one of the parties goes bankrupt before the agreed future date. If the price moves too much in the interim, the parties have to put up additional margin.

To make this more tangible, let's walk through an example where on August 1, you agree to sell me a gallon of milk on September 1. The price of milk on August 1 is $4. If the price of milk is higher than $4 on September 1 then I will make money and if the price is lower then you will make money.

As the buyer, I'll put up $1 of margin of today that will be held by a third party and will pay the remainder of the purchase price on September 1. In the interim, for each $0.50 increase in the price of milk, we agree that I as the buyer will put up another $0.50 in margin. This ensures that if the price doubles to $8, you as the seller aren't taking on too much additional risk that I go bankrupt and fail to pay.

Typical futures contracts are bought using 3-12% margin, meaning that 90%+ of the trade only has to be paid at that future date. You might be able to guess where the story of Amaranth goes from here. Professor Ludwig Chincarini at the University of San Francisco put together a particularly helpful timeline that walks through the whole ordeal. The full paper is linked here for those interested.

Amaranth was betting on natural gas futures, specifically that the price for gas settled in November 2006 would fall in price and those settling in January 2007 would rise in value. And Amaranth bet big - over 70% of all gas futures contracts for November and over 60% of those for January. The magnitude of these trades ensured that if something went wrong and Amaranth needed to sell the contracts, it would be almost impossible.

As you can see in the timeline, it did go wrong. As the prices moved in the wrong direction, Amaranth was required to put up ever-increasing quantities of cash as margin, amounts that quickly overwhelmed how much cash they had available. The hedge fund was forced to sell many of the futures contracts to get access to more cash, causing the prices to move even further in the wrong direction. In the 22 days between August 31 and September 21, Amaranth lost over $4 billion. The hemorrhaging didn't stop until JP Morgan and Citadel, who could meet the increasing margin requirements, bought the remaining futures contracts from the firm in a $2 billion deal.

The scale of the loss rivaled LTCM, yet again the industry solved its own problems. No regulator involvement was even needed to facilitate a deal. JP Morgan and Citadel saw an opportunity to make money at the right price. Amaranth's management and investors took the losses. The system worked as intended.

Sowood

Sowood is a lesson in how the market can stay irrational longer than you can stay solvent. Jeffrey Larson came to fame managing $3 billion of Harvard's endowment before setting off to launch Sowood in 2004. Starting in 2007, Sowood realized the world was not in a good place and anticipated that companies would start to go bankrupt. The hedge fund bought safer, senior debt and sold short more risky, junior debt of public companies. Let's unpack what that means.

In the case of bankruptcy, senior debt gets paid first and junior debt gets paid second only if there is still money left over. Selling short means that Larson borrowed the junior debt, sold it, and then bought it back later to deliver to the lender. If all went well, the price of the debt would fall in between when he borrowed/sold and when he bought it back. He made money by pocketing the difference.

On paper, the strategy looked good. As other investors came to a similar realization that companies would start to go bankrupt they'd buy senior, safer debt and sell riskier, junior debt. Sowood would make money on both. Unfortunately, Larson failed to account for what might happen if everyone needed cash at the same time - everyone sold everything. When there's a rush for cash, sellers often sell the stuff that's easiest to sell. The safer debt was easier to sell and prices cratered.

If Sowood owned the senior debt outright the fund would have taken losses but have lived to fight another day. But Sowood didn't own the debt outright. It was leveraged as much as 12-to-1 making it incredibly vulnerable to large price movements. As the price of the senior debt went down, the banks who lent Sowood money demanded more and more cash as margin. Anticipating how this would eventually play out, Larson sold his funds to the much larger Citadel who could withstand the immediate cash demands.

The final damage? Sowood's two funds lost 55% of their value in a single month, totaling over $1.5 billion in losses. Again, just the investors in Sowood's funds took losses.

Thousands of untold other failures

You may be wondering why we haven't considered Lehman Brothers, Bear Sterns, and the banks that had to be bailed in 2008. While their operations masqueraded as hedge funds, their incentives were a world apart. The people running the "internal" hedge funds at these organizations had little to none of their wealth tied up in the funds; they collected a salary and a bonus and moved on. This perverse incentive structure meant that the investment managers got paid for near-term performance, but the investors were left holding the bag when the internal hedge funds blew up. We now have regulations, most notably the Volcker Rule, that prevents similar structures in the future.

The hedge fund blows-ups we explored were the big ones, the stories that remind us of the damage leverage can do and the speed with which it can act. For every one of these stories, there are thousands of hedge funds that close up shop without so much as a public announcement. In 2019 alone 738 funds were liquidated, but these types of orderly wind-downs don't make the news. They're nonetheless important to keep in mind when analyzing the overall industry and considering legislators railing against "the next hedge fund blow up."

Regulations on the horizon

Against a history of family offices and hedge funds losing massive sums of money without collateral damage, what new legislation was approved by the House Financial Services Committee? The Family Office Regulation Act of 2021 requires family offices managing more than $750 million to register with the Securities and Exchange Commission as exempt reporting advisers. Despite what the name may imply, exempt reporting advisors are still required to publicly report significant information about their investment managers and investments, including how much money they manage.

The Short Sale Transparency and Market Fairness Act requires fund managers managing over $100 million to report their stock holdings monthly instead of the current quarterly and requires that they include their short positions for the first time (reminder: shorting is borrowing to bet on the stock price going down). Combined with the Family Office Act, this would include family offices that have to register as exempt reporting advisors.

With the benefit of having just explored the most dramatic hedge fund blow-ups, we can look at these proposed regulations with a critical eye. Was Archegos even a problem that needed to be addressed? Do the proposed regulations pass the "first, do no harm" test?

Only the family office / hedge funds, their investors, and their banks took losses in the stories we explored. Where the banks did take losses, our existing protections were more than adequate to ensure that they could handle them. Despite protestations from congresswoman Maxine Waters, all of the investors are considered sophisticated, meaning that our regulations permit them to invest in "exempt offerings" that "involve unique risks... [where] you could lose your entire investment." The systemic risk boogeyman - that a bankruptcy would have to be picked up by the taxpayer - claimed by the legislators seems a stretch.

Contrary to the intent of the proposed regulations, both may foster more harm than good. I'm not aware of comparable regulations that require a family to publicly declare their wealth. There is a myriad of structures and methods that would allow families to avoid such disclosures, including moving assets offshore, none of which are healthy for our financial system. Encouraging families to optimize financial structures for privacy rather than investment returns is likely to lead to undesirable outcomes.

More frequent reporting, especially including short sales, has a robust history of abuse. In each of the blow-up examples we discussed earlier, there were other hedge funds on the other side of the trade making money as they found out there was a firm in distress. Once news got out that a hedge fund was in trouble and selling investments to raise cash, hedge funds piled into the trade in an effort to cause prices to go even more out of wack and force the already-in-trouble hedge fund to sell even more. Requiring monthly reporting on short sales gives vulture investors an even greater opportunity to wreak havoc.

Good regulation is good business

This is not an argument against regulation. The increased capital requirements enshrined in the Dodd-Frank Act in the wake of 2008 played a key role in ensuring that banks were able to absorb the losses from Archegos. Margin requirements for futures contracts ensured that the market was warned that Amaranth was running out of cash well before it went bankrupt. These and many others are good, strong regulations that have led to better markets that protect ordinary investors and taxpayer dollars.

This is an argument against misguided attempts to twist the history of orderly bankruptcies to pass novel regulations that are unrelated to the events they propose to prevent. Family offices should be allowed to make poor decisions and lose all of their money. Sophisticated investors should be allowed to invest in hedge funds that blow up.

Most of the money these hedge funds manage comes from pension funds, endowments, and similar organizations that are trying to grow their investments today to pay out the needs of retirees and students tomorrow. We do not know how to create a system that allows fund managers to design novel investment strategies that are risk-free. If we want to continue to encourage fund managers to invent strategies that potentially generate large returns for their investors, we have to accept that blows-ups are part of that invention process.

The best system we know accepts that some investment decisions will be brilliant and others will be stupid. We have strong regulations and need to continue to improve them to mitigate collateral damage. But if we attempt to regulate stupidity out of the system entirely, we're likely to find we'll have lost much of the brilliance as well.

Cocktail Talk

Interested in going deeper on Archegos? Credit Suisse commissioned an external audit that was just published. 170 pages of how badly this went wrong. Includes tidbits like how Archegos didn’t post more margin because they simply chose not to respond to Credit Suisse’s emails.

A controversial fossil that, if real, pushes back back the date of Earth’s earliest known animals to almost 900 million years ago, 350 million years before the Cambrian explosion.

If you haven’t been through LaGuardia Airport recently, you may be surprised that the airport has undergone a dramatic renovation including a new 25 foot tall indoor water fountain. One thing that won’t come as a surprise - $28 dollar beers.

Almost 60 minutes of Elon Musk giving a tour of the Starbase factory. This is apparently part 1 of 3. Even if you’re not excited and nerding out over what SpaceX is building, the fact that a private enterprise is undertaking a build like this is astonishing.

Your Weekly Cocktail

We took our week off from rum drinks last week, which means we’re back at it this week! A classic, courtesy of Barbados.

Corn ‘n’ Oil

1.5oz Bully Boy Rum Cooperative Volume 1

0.5oz Velvet Falernum

2 dashes Angostura Bitters

Pour everything into a mixing glass. Fill 2/3rds with ice or until the alcohol is fully covered. Stir ~50 rotations, about 20 seconds until the glass is frosty. Fill a rocks glass with crushed ice. Pour the booze into the rocks glass and enjoy.

This is a funky one for slow sipping. There aren’t many places for flavors to hide in this drink and they’ll keep on changing as the melting crushed ice brings down the alcohol content. The deep molasses from the rum will give way to a bit more sweetness, amplified by the sugar-heavy Falernum. Clove shines through the whole drink, the main spice note for both Falernum and Angostura bitters. Great way to close out a summer evening.

Cheers,

Jared