Fat Tailed Thoughts: Private Fund Structures

Fat Tailed Thoughts: Private Fund Structures

Hey friends -

Have you ever wondered what a venture capital firm actually is? What's the legal structure? How are they structured to raise money from investors and invest in startups? What does it mean when they say they're "raising a new fund?"

We're going to take a look. As a startup raising money, an investor, or as a general partner, this stuff matters because structure plays a material role in how the fund manager gets paid. As Charlie Munger so eloquently stated:

Show me the incentive and I’ll show you the outcome.

In this week's letter:

Private fund structures: venture capital, hedge funds, private equity, and more

Facts, figures, and links to keep you thinking over a drink

A drink to think it over

Total read time: 20 minutes, 2 seconds.

Alternative Assets

Venture capital, hedge funds, and private equity are all part of a bigger industry, the alternative assets industry. Alternative assets are best defined by what they're not - they're not investable assets that are easy to buy and sell. Easily investable assets are the stuff you’re probably already familiar with: stocks, bonds, US treasuries, and various fund structures like Exchange Traded Funds (ETFs, Mutual Funds) that are combinations of these things. Alternative assets are all the other stuff. Assets and players that are part of the alternatives industry generally have the following characteristics:

There’s some semblance of a market to buy-and-sell the asset, but it's typically quite painful to do so

The buyers and sellers are primarily concerned with the increase in the value of the asset over time, not consuming the asset

The market is big enough that buyers and sellers can move real dollars around (think $1B+ at a minimum)

It turns out this market is big. Over $10 trillion big. And it’s been growing at 20% year-over-year for over a decade.

We're going to focus our exploration on private funds. When you see private fund think “bucket of investors’ money that a general partner is investing.” Everything we’ll walk through is some type of private fund structure. Venture Capital (Funds), Hedge Funds, Private Equity (Funds), Real Estate (Funds), Litigation Finance (Funds), and so on and so forth.

As we'll find out, there are many ways to structure private funds. To understand why we first need to look into why private funds even exist in the first place.

What is the purpose of a private fund?

It's easier to understand private funds by looking at something more familiar that is not a private fund, the ETF. ETFs are exchange traded funds that typically invest in highly liquid assets, meaning they’re easy to convert to cash in large quantities very quickly without affecting the price. As a general rule, fund managers try to match the liquidity of the investment vehicle, such as an ETF, with the underlying assets the fund owns. Mismatches are known as liquidity risk.

The ETFs you’re probably most familiar with are indexed ETFs, meaning the ETF is trying to match the performance of a readily available index such as the S&P 500. The ETF manager achieves this by investing in the same assets with the same portfolio weighting as the index. This is also why the fees for indexed ETFs are typically very low - a lot of this can be automated.

But there’s clearly a limitation here. What if you’re an investor who wants something different?

You want to invest in a fund that invests in illiquid assets like startups or real estate; or,

There’s a brilliant fund manager who wants to invest in normally liquid assets but has a strategy that requires holding on to positions for a long time such as being an activist investor.

Private funds can be great investment vehicles for these purposes.

Private funds: why they exist

There are two major drivers for why private funds exist: returns and regulations.

Returns

It turns out that as an investor, you can often generate better returns in alternatives than you can in traditional, investable assets. But why?

Illiquidity: we all like cash. We can spend cash to buy hamburgers and beer. It’s pretty difficult to buy a Big Mac with shares of a company. Investors can get paid to give up liquidity for some time, such as with a venture capital fund where it may take 10 years or more for the money invested with a venture capital fund in startups to turn back into cash (and hopefully a lot more cash than was put in). You better bet that those investors demand a much higher rate of return for giving up the ability to convert their investment to cash at will.

Risk: often the investments that private funds make are far more “risky” than easily investable assets. Risk is difficult to define but we’ll focus on the most important risk: permanent impairment to principal. Basically, the risk you lose all your money.

Better fund managers: because there is the opportunity to generate better returns, investors tolerate higher fees. This in turn attracts both strong fund managers who can generate better returns and also many laggards attempting to earn higher fees even with subpar performance. So an investor can in-theory access better fund managers, but good luck figuring out who they are before everyone else.

Regulations

So, in short, private funds are high risk, where your money is probably going to be tied up for a long time before you get it back, and it’s super difficult to figure out the good fund managers from the bad ones… and you probably won’t figure it out until you’ve paid way too much in fees anyhow.

To protect investors from taking on risk they don’t fully understand, we have rules limiting who can invest in private funds. Each country has its own set of rules, but the US takes the cake as being the most complicated. Generally, the rules come in two flavors: you must be “sophisticated” and you must have a lot of money.

Sophisticated: this is the squishiest of the requirements. Generally, the rules are written so you have to demonstrate some level of knowledge about the thing you’re investing in and that you have the competency to understand the risks. In the US, this might mean you have a financial services license. In the UK, this might mean you’ve done a lot of business in the past 6 months.

Lots of money: these are generally firmer requirements. The US has a variety of standards including accredited investor, qualified client, and qualified institutional buyer that have varying degrees of qualification. The requirements for an accredited investor are generally the easiest to meet and include individuals with a net worth of $1 million or greater. Other standards like qualified institutional buyer have more onerous requirements, such as requiring corporations to have investments greater than $100 million. Different private funds can be offered to investors based on how they qualify. The point of these requirements is to make sure you’re not going to hurt yourself too badly if you lose all of the money you invest.

If you meet the regulatory requirements, the regulations are relatively straightforward - be prepared to lose all of your money and don’t come complaining when you do as long as it wasn't a fraud. So beyond the illiquidity, risk, and fund managers, what is it that the regulations let you access?

Wider variety of assets: there’s a whole world of stuff that you could invest in that regulators generally won’t let the general public invest in. Startups are a good example, which has a special exemption for employee equity. Art is a less obvious example. Very few people can purchase Picassos directly. Private funds can pool many investors' money to purchase Picassos. The painting itself isn’t regulated, but the private fund is.

Sex appeal: this is the part that’s usually left unsaid but is a major emotional driver. What’s the point of investing in something if everyone else can do it too? Having something interesting to talk about at the cocktail hour, that no one else has access to, plays a big role.

Now that we have a grasp on why private funds exist, let's start exploring how we set them up.

Why are there many private fund structures?

Private funds are typically run by a general partner. It is important to keep in mind that the general partner is a separate company from the private fund. We'll come back to this later on.

The long-term goal of a general partner is to raise money from investors and invest it in assets that will increase in value over time so that the general partner can return more money to the investors than was originally invested. In the meantime, while they're investing the general partner also wants to get paid. With the near and long-term goals in mind, what are the considerations the general partner needs to balance?

Liquidity

The general partner needs to consider investor liquidity. They could allow investors to redeem their money - request it back - or they could lock up the investors' money for a long time. Investor liquidity generally matches the liquidity of the underlying private fund assets. There are two basic private structures to solve for the liquidity match and they pretty much sound like what they are.

Open-end fund: an investor can put money into and request money back out of the private fund when they want. It's rarely “whenever you want” as there are often some limitations around this. Hedge funds that invest in stocks are typically open-ended - they can sell the underlying stocks as needed to generate cash to return back to investors.

Closed-end fund: closed-end funds typically raise money upfront and then close the fund to new investors. Investors don’t get their money back until it is distributed back to them by the general partner. This lock-up period can be 10 years or more, although distributions can happen intermittently throughout the life of the fund. Private equity funds that purchase entire companies, fix them up, and then sell them are typically closed-ended. Same with venture capital funds. It’d be pretty difficult to try to sell a startup to meet an investor redemption request, so the closed-end funds simply don't allow redemptions.

Risk: Liquidity, Bankruptcy, and Litigation

General partners balance many different types of risk. We’re going to focus on just three of them: liquidity, bankruptcy, and litigation.

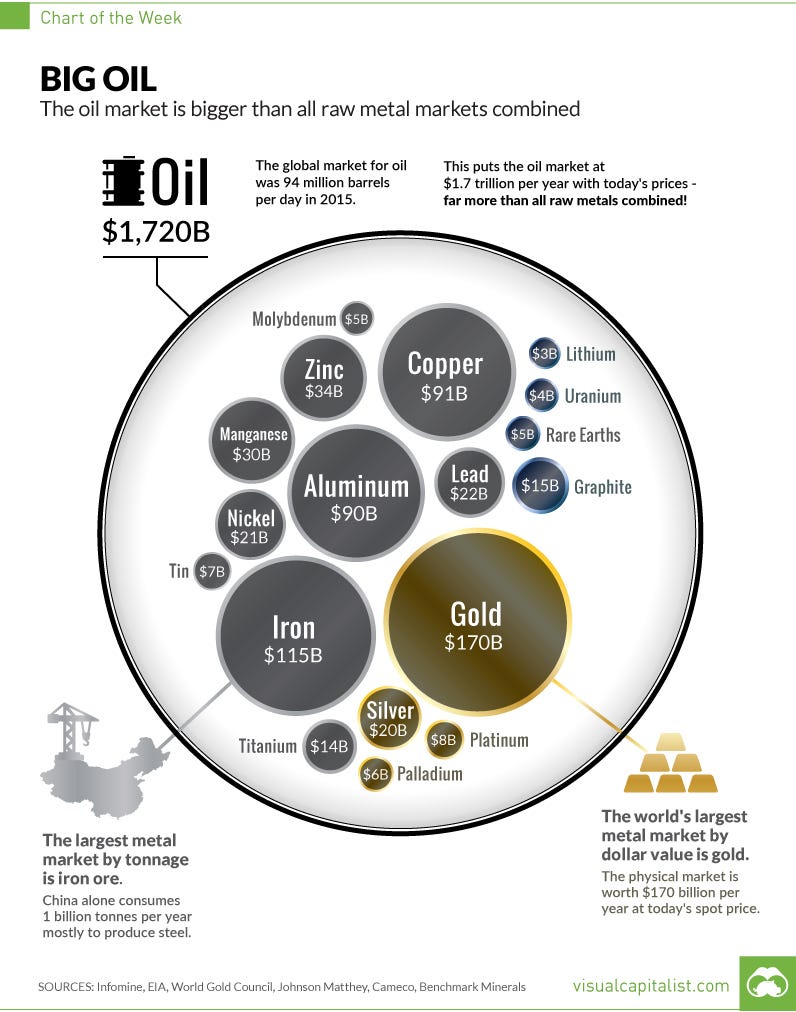

Liquidity risk: remember how we said that even when investors can redeem their money it’s rarely “whenever you want”? One big reason is liquidity risk. Liquidity can be here today and gone tomorrow. Let’s take a fun example that had some truly astounding outcomes. Oil is a big market. A really big market. Like 3x the size of all the metals combined big ($1.7T vs $0.6T as of 2016). Generally, a market that big is highly liquid (reminder: liquid = easy to convert into cash). On April 20th, 2020 the price of oil was -$47 per barrel (you read that correctly, negative $47). This means if you owned a barrel of oil, you had to pay someone $47 to take it off your hands. Ignoring how we got there, which is a fascinating story - it's obvious that oil wasn’t liquid on April 20th.

Bankruptcy risk: this is simply the risk of something going bankrupt. If I’m invested in a lot of stuff, I don’t want any of the investments to go bankrupt and I don’t want my fund to go bankrupt. But I really don’t want a bankruptcy in one part of my portfolio to affect other parts of my portfolio. I need to consider how I protect against bankruptcy at the whole portfolio level.

Litigation risk: this is the risk of getting sued and the associated costs that may come with it. Similar to bankruptcy risk, I want to isolate this risk so that it doesn’t threaten my whole portfolio.

Regulatory Risk

We’ve separated regulatory risk into its own category because a fund rarely gets paid to manage regulatory risk. Liquidity, bankruptcy, and litigation risk are all spectrums that if managed correctly can help produce big returns. Regulatory risk is different and usually existential - get it wrong, and the entire fund can fail. There are rarely “big returns” for doing it right. Regulatory risk has three major considerations, two of which are often in direct opposition to one another. Regulatory risk is always jurisdiction-dependent.

Rule of law: it’s in almost everyone's best interest to have well-written laws that are consistently enforced. Jurisdictions that don’t have established precedent or have corrupt court systems are usually poor places to launch a fund.

Friendliness to the fund: laws can be written in many ways. The general partner will often pick a jurisdiction where the laws favor the fund and the general partner in disputes rather than the investor.

Global status: this is usually in direct opposition to “friendliness.” Fund-friendly jurisdictions walk a tightrope of being generally lenient and favorable to the fund, while still not getting on the wrong side of places like the US that want to crack down on money laundering and tax evasion.

Taxes

Taxes are relatively straightforward in principle but devilishly difficult in practice. Tax is largely dependent on jurisdiction which is slightly different than geography. Whereas geography is a physical location, jurisdiction is the area over which a given regulator has authority. Jurisdictions can overlap leading to turf wars between regulators. We’re going to highlight a couple of the inputs to tax considerations.

Taxes owed by the general partner: the general partner typically wants to lower their taxes. They’ll want to locate in a jurisdiction that’s “tax-advantaged” and choose a legal structure to match such as a Limited Liability Company (LLC) or Limited Partner (LP). A major consideration is how the monies paid to the general partner will be treated under the tax law. Are they long-term capital gains, income, or something else entirely? And how are those taxed?

Taxes owed by the fund: the general partner makes most of their money based on the success of the fund. The fewer taxes the fund pays, the more money the general partner makes. The general partner is going to be very diligent to ensure the fund is “tax-advantaged” as well, similar to what the general partner does for itself.

Taxes owed by the investors: taxes can make a material difference to the net performance realized by the investor. Net performance is the take-home returns after fees, taxes, and all the other costs. There’s a lot that goes into this, but the fundamental considerations are similar to those of the GP: jurisdiction, legal structure, and how monies paid are treated.

If you ever see the term “off-shore” just think “tax-friendly for the fund.” The term comes from the fact that even though most of everything may actually be happening in the US or Europe or similar (“on-shore”), the legal address of the fund is someplace else like the Cayman Islands (“off-shore”).

Fees & Expenses

Always save the best for last - the general partner needs to get paid! The two primary ways they get paid are based on the value of the assets they manage and how much they increase the value of those assets. Part of getting paid is also keeping operating expenses low.

Management Fee: general partners typically charge a flat management fee based on a percentage of the assets under management of the private fund. 1-2% is typical. The fee is charged from the general partner to the private fund.

Performance Fee: when the private fund increases in value, the general partner gets paid considerably more. 10-20% of profits is typical and can go much higher, such as The Medallion Fund which charges a 44% performance fee. Sometimes the performance will be subject to a hurdle rate which means the fee is only paid if the annual return of the private fund is higher than the hurdle rate. The hurdle rate can be fixed such as 5% a year or it can be a benchmark such as the S&P 500 index. Some funds also include a high-water mark which ensures the general partner only gets paid for increasing the long-term value of the fund, not for recouping earlier losses. You may hear the term carried interest for private equity and venture capital. It works similarly to the performance fee.

Expenses: the general partner usually has significant discretion over who pays expenses. Either the general partner can pay or they can charge the expense to the private fund. Expenses paid by the general partner come out of the general partner's money. Expenses paid by the private fund get paid for by the investors. It's not hard to guess where it usually gets charged.

That's a lot of moving parts. When setting up the private fund, the general partner has to balance among these many considerations to create a structure that will be attractive for both the general partner and the investors. Let's explore what those structures are.

Private funds structures

Private fund structures can get complex. Rather than dive immediately into the details, we're going to briefly look at the many different structuring options at our disposal. Think of these as lego blocks that can be combined and recombined in many different ways to create novel structures that optimize for whatever it is we want to accomplish.

Private Fund Structural Options

Private funds: many, many paragraphs later we’re finally getting a definition. A private fund is a company. When the investors invest in the private fund, they’re actually purchasing shares of the company in a manner, not all that different than if they invested in Apple or Tesla. The most common legal structure for private funds is Limited Liability Companies (LLCs) and Limited Partnerships (LPs). If you've ever heard of an investor in a private fund called a "limited partner," this is where that term comes from.

A general partner may in fact run many private funds, i.e. many separate companies. When we think of a major venture capital firm like Sequoia or a large hedge fund like Bridgewater, there are in fact many private funds under the brand umbrella. When you hear that Sequoia raised $195 million for a new fund, what they've actually done is start a new company under the Sequoia brand managed by the Sequoia general partner. Sometimes we call these collections of funds fund families or parallel funds.

Classes: shares in the private fund can be split up into one or more classes. Classes are used to distinguish rights or other investor concerns among shareholders. Typical uses of classes include different fee amounts per class, investing in different currencies, and different minimum investment amounts.

Management company: while we've been calling the general partner a single company, we can actually split it into two different companies. Company 1 is the general partner we described earlier and is responsible for advising the private fund(s) on what to invest in. Company 1 receives the performance fee. Company 2 is a management company responsible for managing the private fund - actually executing the investments, working with the startups if it's a venture capital firm, and whatever else Company 1 advises it to do. Company 2 receives the management fees.

Master-Feeder funds: general partners will want to allow investors from multiple countries to invest. One way of structuring this that is often tax-advantaged for the investors is using master-feeder funds. The master fund is the private fund doing the actual investing, typically based in a low-tax jurisdiction. The feeder funds are located in jurisdictions that make sense for the investors the general partner is trying to attract, such as a US-based feeder fund for US investors. Investors own shares of the feeder funds, which in turn own shares of the master fund.

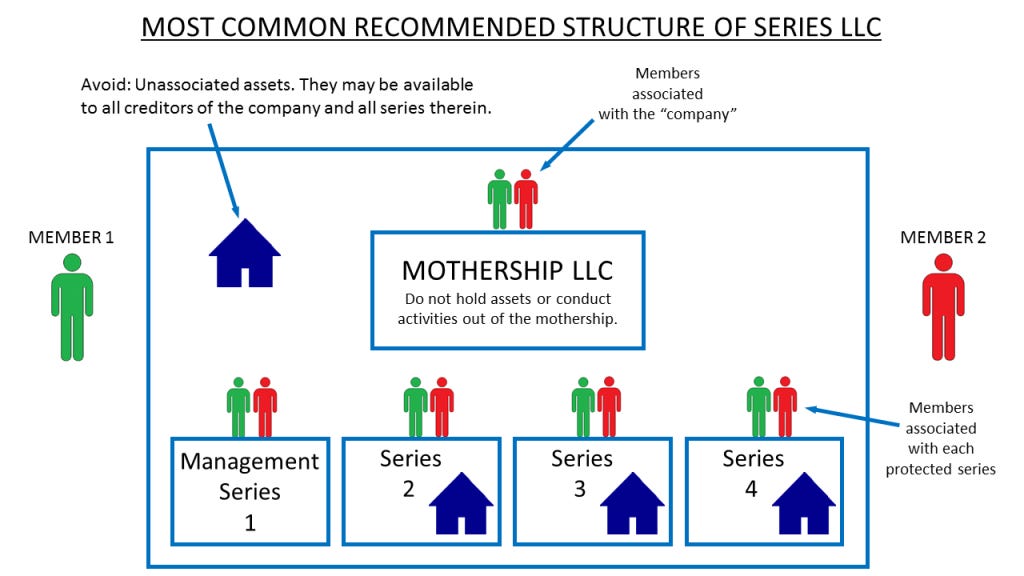

Series LLC: this is a relatively new innovation only recognized today in 8 states plus Puerto Rico. A series is a group of entities under a single limited liability company where the entities are bankruptcy remote from each other. Many startups enabling fractional ownership of real estate and collectibles like comic books are set up as series LLCs where each asset is its own series.

Example Private Fund Structures

We're finally ready to structure some private funds. What follows are common examples of how funds can be structured, but note that the varieties are nearly endless and remain a key point of innovation in the industry.

Single Fund, Closed End

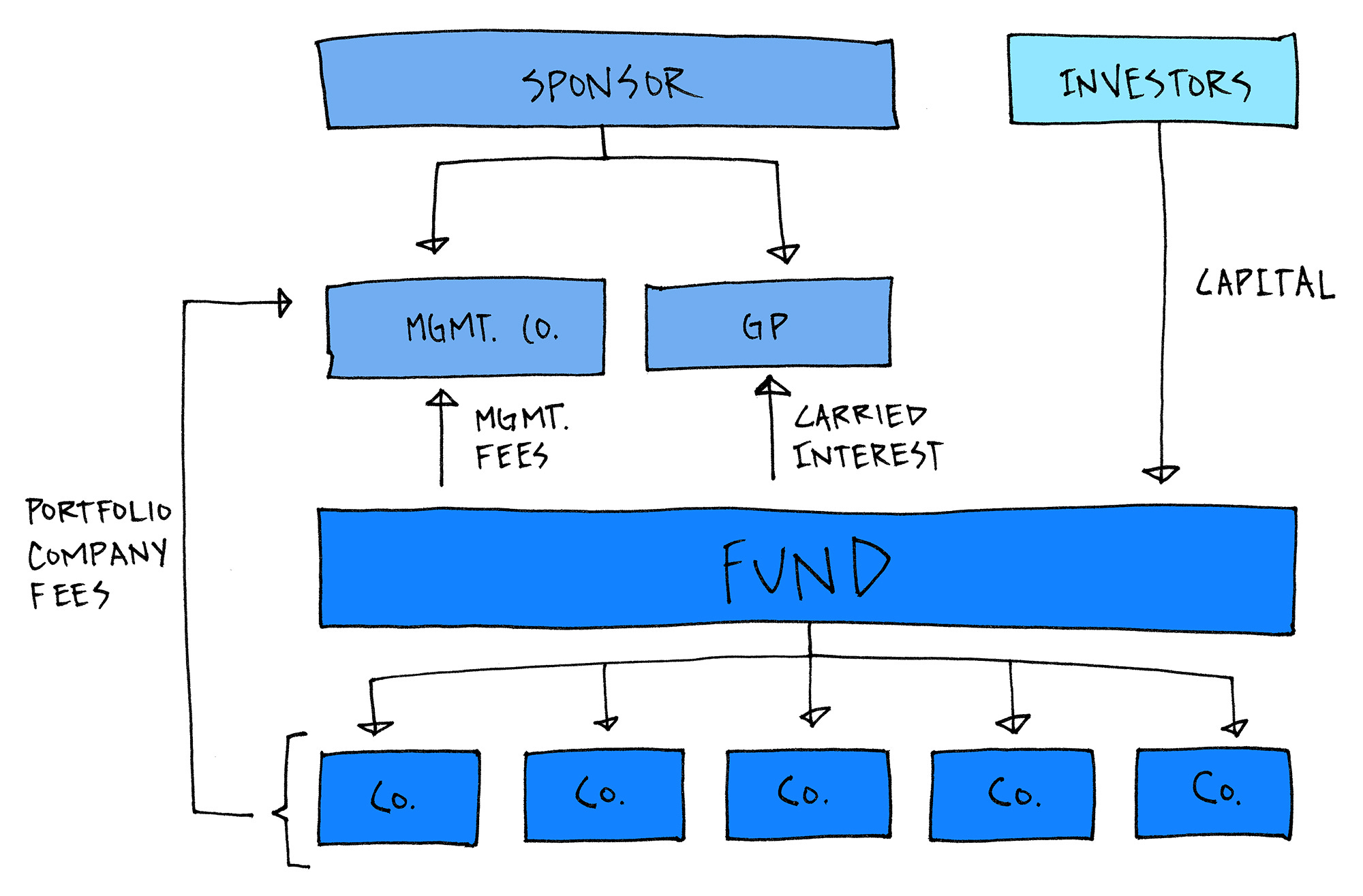

This is a vanilla closed-end structure with a single fund. This is about as simple as private equity and venture capital can get.

Investors put their money into the fund

They commit to invest but don’t put all their money in at once

As the general partner requests the money to be delivered through capital calls, the investors send the money

The fund invests the money in whatever they said they would, like investing in startups

Management Company gets paid fees by the fund for managing the fund

Management Company can get paid even more fees by the companies it invests if it provides other services

Not listed here, but the Management Company may also lend money to the companies it invests in for yet more fees

When the fund sells the companies, the fund distributes the profits to investors and the general partner receives its performance fees

Note that we haven't discussed the “Sponsor.” The sponsor is typically made up of the general partner and the management company. This is a bit misleading because often the general partner and management company are also exactly the same people, just working for multiple companies. When we use the terms venture capital firm or hedge funds or the like, we usually mean the total collection of general partner + management company + sponsor.

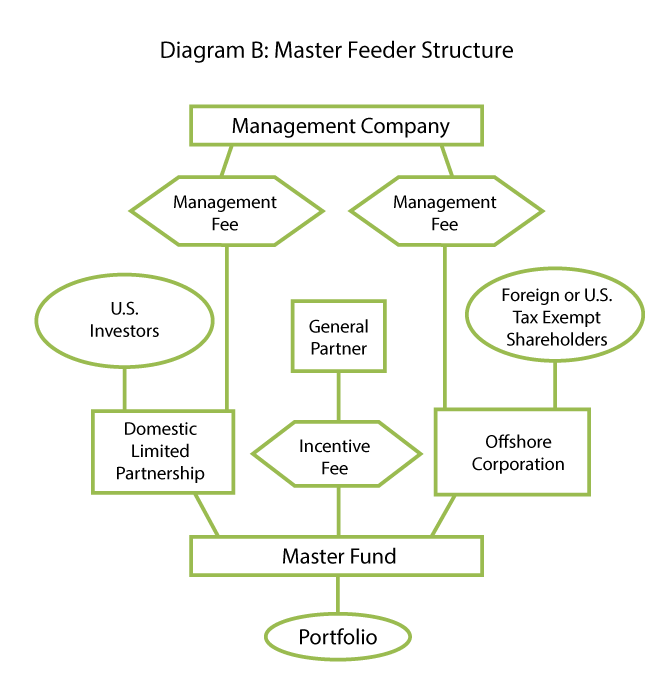

Master-Feeder

Master-Feeder structures can get a little funky, but the basic idea is straightforward.

US investors purchase shares of a private fund called Domestic Limited Partnership based in the US

Management Co charges Domestic Limited Partnership for managing the money

Non-US investors purchase shares in a different private fund called Offshore Corporation, probably based in the Cayman Islands or other low tax jurisdiction

Management Co also charges Offshore Corporation for managing the money

Domestic Limited Partnership and Offshore Corporation both purchase shares in a third private fund, Master Fund, likely also based in the Cayman Islands

Master Fund does the actual investing into investable assets like startups

General Partner charges Master Fund for advising on the investments

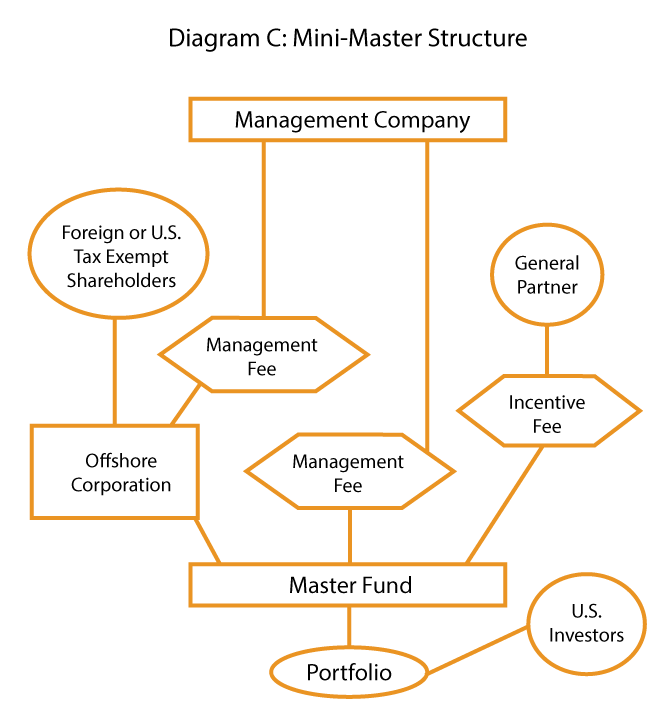

Mini-Master

The Mini-Master structure is a variation of the Master-Feeder structure. It similarly allows non-US investors to avoid US taxes and can allow the general partner to lower the taxes it pays on the management and performance fees.

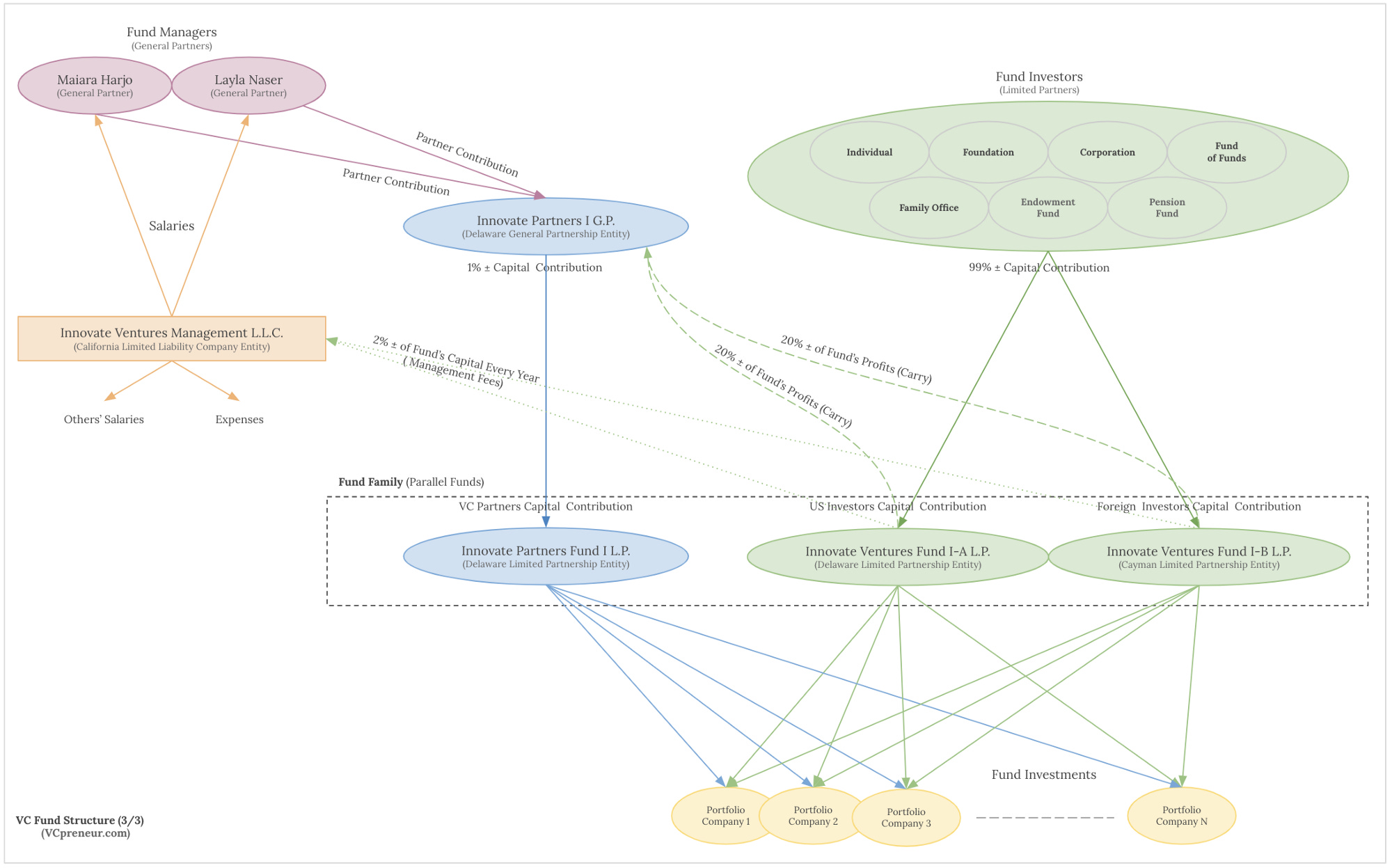

Parallel Funds

A Parallel Fund Structure means you have multiple separate private funds (reminder: separate companies) investing alongside each other. If we play out the various combinations of who gets paid and who invests, this is what it can start to look like. Notice a couple of things:

The general partners are in fact three different things and getting paid three different ways:

Salaried employees of Management Co, collecting the Management Fee

Partners in General Partner Co, collecting the Carried Interest

Direct Investors in the portfolio companies, getting the same returns as the investors when they sell the portfolio companies

This is set up as parallel funds, not as a master-feeder

US fund for US investors based in Delaware

Offshore fund for non-US investors based in the Cayman Islands

Series LLC

Series LLCs are a relatively recent innovation that really took hold in real estate first. There are two approaches of structuring them.

In the first approach, each investor owns shares in the parent LLC and can choose in which of the underlying Series to invest (one, some, or all). This allows investors to have lots of flexibility about investing in one series versus another while reducing the general partner's expenses in managing multiple separate private funds.

In the second approach, each investor owns shares in the parent LLC and the parent LLC itself owns the shares in each of the Series (meaning that investors own all of the Series). This gives the general partner more control over how to allocate investors' monies across the investable assets while continuing to protect each asset. In real estate in particular, where you might want a general partner who acquires lots of buildings but are concerned about how a bankruptcy of any one building could lead to litigation for the whole fund, this can be an attractive structure.

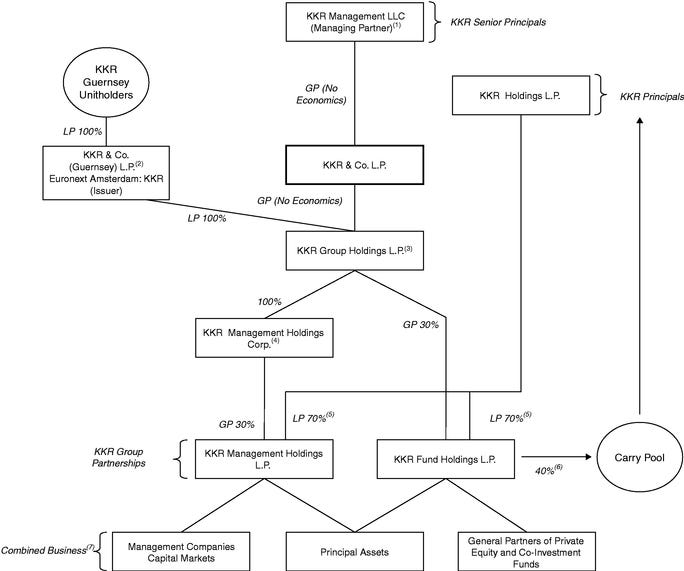

Just for Fun - KKR, Public Private Equity Firm

KKR (ticker: KKR) is a publicly listed private equity firm. You can go buy shares in KKR just like you would shares in Apple or another company, but you have to be one of those qualified investors (sophisticated and rich) to invest directly in the funds. The diagrams above are from annual reports. This should give you a sense of just how complex these structures can get when we start to mix and match.

Why should I care about fund structure?

If you ever accept money from a venture capital firm or other private funds, have the opportunity to invest with one, or maybe are thinking about starting one, this stuff matters. As a startup, understanding how the general partner makes money helps you understand their incentives and how that informs your capital raise.

As an investor, the structure can tell you a lot about wether the general partner is trying to make you money or line their pockets at your expense. The structure also materially informs your tax and legal liabilities.

If you're thinking about starting a private fund, there's a huge space for exploring new structures that can unlock new business models. Look at what Otis is doing for fractional ownership of comic books and Edly is doing to finance student education. Both are structured as series LLCs and able to move much faster than their peers at a lower cost to make new investment opportunities available to investors.

These types of details can be dry at times, but that makes them all the more important. This isn't the sexy stuff about finding the next great investment and making deals. It often gets ignored. That's often exactly where new opportunity lies.

Cocktail Talk

Can't say I saw this coming. I don't think the bird did either. It turns out the slow, lumbering giant tortoise is actually a hunter. We don't even have a basic understanding of this, such as if a tortoise can even digest a baby bird. Can't wait to see the inevitable Ph.D. thesis defense on feeding meat to herbivores.

The NY Times put together an incredible expose on hospital prices. Not only are some procedures cheaper if you don't use insurance, the US started requiring hospitals to publish the prices of hospital services this year and most hospitals are simply refusing to do so. The $100,000 maximum fine against hospitals is pennies compared to the billions of dollars many of them make a year.

The more experiments we do, the more we find out just how awesome Einstein was. One of his major theories was just confirmed by experimental evidence. It turns out that if energy and mass are equivalent, not only can we create energy from mass but we can also create mass from energy. By colliding high-energy photons, we successfully created a new mass where there was none before.

Two weeks ago, we highlighted that $610 million worth of cryptocurrencies were stolen by a hacker who exploited a bug in a decentralized finance application on a public blockchain. In a wild conclusion to the story, all $610 million has been returned. While the company that built the blockchain has stated that they do not intend to press charges, it remains as yet unknown if others will attempt to do so.

Did you know that all of the livestock on earth collectively weighs almost 20x more than all of us humans? And bacteria are another 700x heavier than livestock. Check out this awesome visualization put together by Visual Capitalist for these comparisons and more.

Your Weekly Cocktail

Watch out - this one packs a wallop.

Mississippi

2.0oz Pierre Ferrand 1840 Formula Cognac

1.0oz Bourbon

1.0oz Dark Rum

0.5oz Lemon Juice

0.5oz Simple Syrup

Pour all of the ingredients into a shaker. Fill with ice until the alcohol is covered. Shake for ~20 seconds, until the outside of the shaker is frosty. Fill a rocks glass with cracked ice, strain into the rocks glass, and strap yourself in.

This is… a ridiculous drink. Cocktail historian David Wondrich traced the original recipe for this back to Bon Vivant's Companion, published in 1862 (!!). What’s most surprising is that despite the absurd quantities of alcohol and almost complete lack of anything else, it’s nonetheless a wonderful drink. Watch out though, this one will sneak up on you if you’re not paying attention.

Cheers,

Jared

Awesome writeup . Always wondered how private funds are set up. This gives a very clear picture. Thanks a lot.