Fat Tailed Thoughts: Startup Equity Compensation

Hey friends -

Over the past few weeks one topic keeps coming up in conversation, on Twitter and in person - how should startup employees think about startup equity? It's an important question where seemingly small structural differences can have massive implications for long-term value. Hopefully, this letter gives you a more nuanced understanding that helps inform your future decisions. This is the guide I wish I had.

In this week's letter:

Startup equity: what is it, how should employees value it, and what are the ways it can be structured?

Facts, figures, and links to keep you thinking over a drink

A drink to think it over

Standard disclaimer - I'm not a lawyer, tax expert, or any of the other professionals you should engage when you're entering into contracts or making material financial decisions. Recommended that you engage an appropriate professional to understand your own personal situation.

Total read time: 15 minutes, 29 seconds.

Startup Equity Compensation

Startup equity has many moving parts. We're going to explore it from the perspective of an employee at a US startup, starting with the major considerations including timing and opportunity cost. From there we'll look at the many ways equity can be structured and the tradeoffs among the structures.

Before we go too much further, let's define what we're discussing: equity is partial ownership of a company, also known as stock in the company. We're specifically discussing equity compensation, the equity you earn from working for the company.

Don’t want to go too deep into the details? Jump to the handy summary table at the end.

What should I be thinking about?

Firstly - if someone is offering you equity to work at a startup, congratulations! That means the people hiring you think you're valuable and want to pay you for the value you're going to bring to the company.

Once you've taken a moment to recognize your accomplishment, the foremost consideration is to recognize that the startup could compensate you in many other ways. You could get more cash through a bigger salary, you could have use of a company car, or the company could send you a year's supply of Skittles candies at the start of every year.

By accepting the startup equity instead, you're forgoing other forms of compensation you could receive at other companies. This opportunity cost is very real. That means you should think seriously about the equity - is it more valuable than the opportunity cost?

To figure out value, we have to explore other considerations. The biggest is whether or not the company will succeed at all. If we assume it'll be successful, we still need to look at equity compensation structure, timing, cost, and liquidity.

Structure

More often than not, you won't receive equity directly. Instead, the startup will propose a structure where you earn equity in the future. There are three common structures:

Restricted stock awards - stock you take ownership of today that is subject to restrictions,

Options - the right to purchase stock in the future at a price determined today, and

Restricted stock units - an agreement from the company to issue you shares or the cash value of shares at a future date.

These are contractual agreements for future equity, not equity today. This is a critical distinction because while equity is something you can own and (generally) cannot be taken away from you, a contract can include a bunch of terms about when you'll receive the equity and how you can lose it. Different structures can also have wildly different legal and tax considerations.

Let's explore the other considerations before we go too much deeper into the structures.

Timing

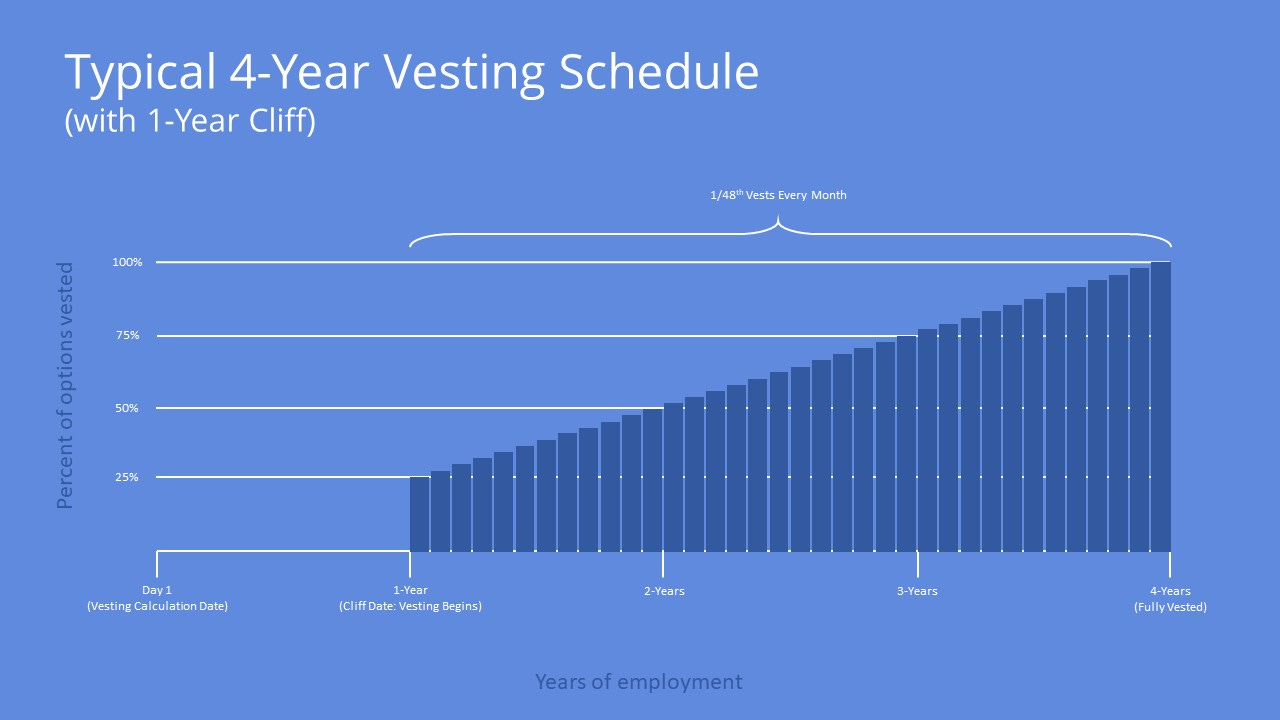

Timing is the second major consideration, starting with when you earn the equity. You'll most likely earn equity on a vesting schedule. Vesting is the process by which you gain rights to the equity and can be done on a regular schedule, such as monthly, or tied to specific performance milestones. In short, the equity isn't yours until it vests. Vesting will often include a cliff, which means that the equity isn't yours until after a designated length of time.

A common compensation setup is "monthly vesting over four years with a one-year cliff." The first part of this - monthly vesting over four years - means that you'll earn 1/48th of your equity compensation every month for four years. The second part of this - with a one-year cliff - means that you earn nothing until the end of year 1, at which point you receive the entire 25% of year one's equity. Take a look at the graph below to see how this plays out.

The flip side of when you earn equity is when you forfeit equity. If you leave the startup before your vesting schedule concludes, you'll typically forfeit any unearned equity compensation. Even if your equity compensation is vested, you may forfeit the compensation when you leave the company. Why might this happen? It comes down to cost.

Cost

Cost shows up twice - the cash outlay required to obtain the equity and the cash owed to the taxman. Some equity compensation structures require that you purchase the equity, such as options. We'll go in-depth on these structures in a bit.

All equity compensation plans are subject to taxes. The amount and timing of taxes owed varies depending on how the equity compensation is structured, and tax breaks can materially decrease and even eliminate taxes owed. We'll look into tax treatment when we go deeper into equity structures. This will be the most complex topic we explore.

Liquidity

While liquidity is a big subject in its own right, for startup employees we're just concerned with the ability to convert the startup equity to cash. Historically, you could only convert your equity to cash when the startup was acquired or when the startup became a public company and you sold your shares.

Today, startups are increasingly supporting two types of liquidity programs for employees while the startup remains private: facilitating employee equity sales so that employees can sell their shares and facilitating loans against employee equity so that the employees can receive cash and still keep their equity. Fair warning: both programs are relatively new and transactional fees remain high. The programs may nonetheless be attractive for employees who need cash today.

I'm thinking about...

Pulling this all together, we're thinking about 4 major considerations: structure, timing, cost, and liquidity:

Structure is how you obtain the equity and the major determining factor for the other three considerations and what we'll dive into from here,

Timing is important both for when you earn equity compensation as well as when you might forfeit it,

Cost matters both for the cash you may have to spend to actually own the equity as well as the taxes you may owe, and

Liquidity is your ability to convert that hard-earned equity compensation to something you can spend at the grocery store.

I've left out one other major consideration - share class. Whereas employees receive common equity, investors typically receive preferred equity. Preferred equity is what it sounds like - equity where the ownership rights are better than those of common equity.

There can be many classes of preferred equity each with different rights. Some rights can "stack," where one class of preferred equity can be "more" preferred than another, and other rights can be universal to all preferred equity holders. This is an important topic, but few employees will be eligible for preferred equity or even have access to the terms so we've left it out of our considerations here. We may come back to it in a future letter.

With this grounding of how to think about startup equity compensation, let's explore the structures.

Equity Compensation Structures

We'll stay focused on our three main types of equity compensation in the US - restricted stock awards, options, and restricted stock units. Keep in mind that this is by no means an exhaustive list. There are other less common structures including warrants and phantom stock that are generally less advantageous to employees but maybe attractive under certain scenarios.

For each structure, we'll look at how they work, the tax implications, and when you're most likely to encounter them.

Restricted Stock Awards (RSAs)

Restricted stock awards (RSAs) are for stock that you take ownership of now, but the stock comes with restrictions. A typical restriction is vesting, which is a bit of a misnomer because stock you already own can't be taken away from you. In this case, it's repurchased. As the restricted stock vests, the startup has the right to repurchase less and less of the stock back from you until their repurchase rights expire entirely. This model ensures that if you receive a lot of stock awards and then leave the company soon-thereafter, the company can buy back the stock from you.

While not typically expressed this way, you are actually selling valuable options back to the company. You're selling the company the right to purchase the shares from you at a future point in time at today's price. Framed as a sale rather than as a restriction appropriately frames just how valuable these options really are. How much would you pay for the right to purchase shares in a highly promising startup at yesterday's price?

Tax Basics for RSAs

The taxes you owe are dependent on how you take ownership of the shares. Depending on how the RSA is structured, you may be able to purchase the stock at the current value, at a discount to the current value, or at no cost at all. Let's look at the taxes for each of these in turn before we layer in more complex scenarios:

Purchase at current value: you don't owe any taxes at purchase because the purchase price = the current value so there's no "compensation" to be taxed

Purchase at a discounted value: you owe ordinary income taxes on the difference between the current valuation minus the purchase price

Purchase at zero cost: you owe ordinary income taxes on the entire current value of the shares (effectively current valuation minus zero)

Current value is typically determined through a 490A valuation, an equity value appraisal conducted by a third party that the IRS accepts as a fair basis for value. The current per-share value will likely be less than what investors pay because the value of the common equity you're receiving is less than the value of the preferred equity the investors purchased.

Do keep in mind that if the excess value you receive (current valuation minus purchase price) is large compared to your salary, it could push you into a higher ordinary income tax bracket. On the bright side, as long as you own the shares for more than a year, you'll only owe capital gains taxes (~20%) when you eventually sell.

Complicating Factors for RSA Taxes

Now let's layer in the complicating factors. Complicating factor #1 is a vesting schedule. If your RSAs are subject to a vesting schedule, you typically won't purchase the shares or owe taxes until they vest. While putting off paying taxes may seem like a good thing, the increased amount of taxes typically overwhelms any benefit of paying later.

Complicating factor #2 works to your advantage: the 83(b) election. The IRS allows you to purchase shares even if they haven't vested and pay the ordinary income taxes on them now. Why would you do that? Because the IRS makes it worth your while: you owe zero additional taxes when the RSAs vest and you owe zero capital gains taxes on the first $10 million in gains from when you sell the shares. The qualification requirements are that you make the election within 30 days of receiving the equity (the grant date not the vesting date), hold the shares for at least a year, and that the startup is worth less than $50 million. All it takes is a one-page form.

Other Considerations for RSAs

The RSA structure means that you're a shareholder in the fullest sense. You're entitled to dividends, voting rights, and anything else that comes with common equity. Once the shares have fully vested, you can also borrow against or sell the shares subject to the controls the company has in place for all common shareholders. If you leave the company, the shares come with you.

Because of the cost to purchase the stock at current value or the big tax bills, RSAs are common only in the early days of a startup when the valuation is low. As the valuation increases, RSAs can result in employees getting stuck with tax bills that are many times larger than their salaries. One popular way to solve that problem is options.

Options (ISOs, NSOs)

Options give you the right, but not the obligation, to purchase equity at a future date for a price determined today. That price is known as the strike price. Like RSAs, most options will be subject to a vesting plan meaning that you will be promised options today and earn them during your employment. You don't actually own the equity until you exercise the options.

Exercising the option is the term for when you exercise your right to purchase the equity at the previously agreed-upon price. Startups will often allow you to do a cashless exercise where you sell some of your options back to the company to pay to purchase the rest. The term cashless comes from the fact that no cash actually exchanges hands, just the options. Let's walk through an example to understand the tradeoffs with a cashless exercise:

Timmy owns options entitling him to purchase 10 shares at a strike price of $2 per share. The company's current valuation for common equity per the 490A valuation is $4 per share. There are three ways he can obtain the underlying shares:

Timmy can spend the $20 ($2 per share x 10 shares) and take ownership of $40 worth of equity ($4 per share x 10 shares) for a total gain of $20.

Timmy can cashless exercise today - sell 5 of the options back to the company to generate $20 ($4 per share x 5 shares) and then use the $20 to purchase the remaining 5 shares. He's left with $20 worth of shares, also a gain of $20.

Timmy can cashless exercise in the future and hope the share price goes up in the meantime. As the price goes up, he will have to sell fewer shares to pay for the rest. For instance, if the price goes up to $5, he will only have to sell 4 shares and will get to keep 6.

Tax Basics for Options

Like with RSAs, ordinary income taxes are calculated based on that difference between the current share value and the strike price. The amount of taxes actually owed is complex because there are two types of options - Incentive Stock Options (ISOs) and Non-Qualifying Stock Options (NSOs). We'll go through the details of each and then walk through an example.

ISOs are only available to employees. You can avoid up to $100,000 per year in taxes if you meet the requirements:

You hold the ISO for at least two years after the grant date,

You hold the shares for at least one year after the exercise date, and

You are still an employee or departed the company no more than three months ago.

If you fail any of the above requirements then the options convert to NSOs. If the ISOs total exercisable value in a tax year exceeds $100,000, the "excess" options also convert to NSOs.

NSOs are a simpler construct. Their options just like ISOs, but there’s no tax avoidance - you owe ordinary income tax on the full difference between the current share value and the strike price.

After you exercise the options to take ownership of the shares, you will still owe additional taxes when you sell the shares if the price of the shares goes up. If you sell the shares within a year of owning them, you owe additional ordinary income tax on the additional gain. If you hold the shares for at least a year before selling, then you owe long-term capital gains taxes when you sell.

This is a lot of moving parts. Let's walk through another example. Sally receives an equity compensation plan for ISOs entitling her to purchase 100,000 shares at a strike price of $2 per share. The plan vests over 4 years with a one-year cliff, so she will earn 25,000 options per year. The company's per-share valuation is $10 per share:

At the end of year 1, Sally will receive 25,000 options worth $200,000. The first 12,500 options are ISOs and the remaining options convert to NSOs.

During the next 24 months, Sally receives another 50,000 options. The options received in the first six months of each tax year are ISOs and the options received in the second six months of each tax year are NSOs.

At the start of year 4, Sally decides to exercise all 25,000 of her year 1 options and leave the company. She owes no taxes on the ISOs and owes ordinary income tax on the $100,000 gain from exercising the NSOs. She forfeits the remaining 25,000 options that she would have earned in year 4.

Three months into year 4, all of Sally's remaining ISOs from years 2 and 3 convert to NSOs.

Six months into year 4, Sally decides to sell 20,000 shares she owns from previously exercising her options. She sells at $10 per share. Sally owes no additional taxes on the 12,500 shares from NSOs. The 7,500 shares from ISOs no longer qualify for the tax savings because she did not hold them for at least a year, so she owes ordinary income tax on the original $60,000 gain (7,500 x ($10 - $2)).

At the start of year 5, Sally decides to sell her remaining 5,000 shares at $12 per share. She only owes taxes on the additional $10,000 gain (from $10 to $12 per share). The $10,000 gain is taxed as long-term capital gains. She still owns another 50,000 NSOs that haven't been exercised.

Complicating Factors for Options Taxes

Complicating factor #1 is the alternative minimum tax. The alternative minimum tax is a different way the IRS calculates the total taxes owed in a tax year and includes the full gain (current share value minus strike price) at the time of exercise to determine the taxes owed. You don't get a break on the $100,000 of ISO gains for the purpose of the calculation. If the taxes you owe through the ordinary income tax calculation is below the floor rate using the alternative minimum tax calculation, then you'll end up paying the alternative minimum tax.

Complicating factor #2 is again the 83(b) election. Similar to RSAs you can early exercise your options, meaning you can exercise the options before they vest. By filing an 83(b) election you will owe zero capital gains taxes on the first $10 million in gains from when you eventually sell the shares, subject to the same requirements as with the RSAs.

Other Considerations for Options

Until you exercise the options, the shares are not yours. You don't get any of the rights that come along with the shares. This means that options can be subject to a wide variety of restrictions that the company embeds in the options contract. One common restriction is that employees will forfeit their options shortly after they leave the company even if they are already vested. Another common restriction prevents employees from selling or borrowing against the options. These and similar constraints are solved by exercising the options and taking ownership of the actual shares.

ISOs and NSOs are also subject to a 10 year expiration from grate date if not exercised. Expiration here means you forfeit the options entirely. 10 years might sound like a long time, but the median time for a startup to go public is more than 11 years.

As startups become more valuable, the cost to exercise options and associated taxes can become prohibitive. Restricted Stock Units can become a more attractive construct.

Restricted Stock Units (RSUs)

This one is thankfully simpler. Restricted stock units (RSUs) are an agreement from the company to issue you shares or the cash value of shares at a future date.

Tax Basics for RSUs

RSUs are treated as ordinary income. You owe ordinary income tax on the full value of the shares as calculated from when they vest. Many startups will withhold shares to pay for taxes, similar to how the company already withholds income to pay for income taxes.

If you hold the shares for less than a year before selling, you'll owe additional ordinary income tax on the difference between the price when you received the shares and the sale price. If you hold the shares for more than a year, then the tax becomes long-term capital gains.

Tax Complications for RSUs

Not a lot! They're not eligible for an 83(b) election and they won't trigger the alternative minimum tax. Do keep in mind that if the company does not withhold shares to help offset taxes, you could end up scrambling for cash to pay a very large tax bill when the shares vest.

Other Considerations for RSUs

Similar to options, this is just a contract between you and the company. The company can put many restrictions into the contract. Once the RSU vests and you take ownership of the actual shares, you escape the constraints of the contract and get all the rights of a common shareholder.

These are most common in late-stage startups. Often the vesting schedule will be tied to events such as an acquisition or an IPO where you'll have an opportunity to sell the shares or receive cash instead. Tying the vesting schedule to such liquidation events ensures you'll be able to pay the associated taxes.

Comparison of Equity Structures

That was a whirlwind tour. I encourage you to refer back to the relevant sections for details. For a quick glance view, check out the table below.

It would be remiss of me not to mention the Holloway Guide to Equity Compensation. At a hefty 80 pages, it covers many of the topics here in greater depth and links out over 350 additional resources. To the best of my knowledge, it is the most robust coverage of the topic of which I'm aware.

I hope this guide is helpful as you think about equity compensation in the future.

Cocktail Talk

If you're familiar with Lyme disease, you know how terrible it can be. Cases have been growing rapidly in recent years to over 500,000 cases a year. Hope may be on the horizon. A phase-one human trial just kicked off for an annual preventative dose.

A wide-ranging investigation into nameless, almost tasteless street food that’s nonetheless found all over India. Unbelievably, it has an almost unknown plant origin. One intrepid journalist uncovered where it actually comes from.

JP Koning put together a very cool photo essay on the Spanish dollar. Forged from silver brought over from the New World, the Spanish dollar was at one point a near-ubiquitous form of currency, so much so that England re-stamped the coins with their own king’s profile. You may be more familiar with the coin’s other name: pieces of eight.

Ever wondered about the life of woolly mammoths? Scientists discovered that one male wandered a distance equivalent to twice the circumference of the earth during his life. The discovery was made by analyzing geochemical isotopes still present in the 28-year-old male's tusks over 17,000 years later.

Your Weekly Cocktail

A hot weather drink well off the beaten path.

Jasmine

1.5oz Plymouth Gin

1.0oz Cointreau

0.5oz Campari

0.75oz Lemon juice

Pour all of the ingredients into a shaker. Fill with ice until the alcohol is covered. Shake for ~20 seconds, until the outside of the shaker is frosty. Strain into a rocks glass (or a coupe if you’ve got it) and enjoy!

This is a weird one. Campari is difficult to tame but this drink manages it - it blends in beautifully without needing overproof alcohol or too much sweet to bring it into line. It’s at once sweet from the Cointreau, floral from the gin and Campari, and bitter from the Campari and lemon juice. All the notes you want for a stoop cocktail on a hot summer’s day.

Cheers,

Jared

A solid rundown of different structures, as sort of an equity-comp 101. But the question most people have a very hard time assessing is, what is a fair award for an employee, based on role, seniority, and company maturity? The best analyses and summaries of what is "market rate" for that are many years old, in some cases a decade old. There's just not a lot of info on that out there, and I think you'd be doing a big service to compile some ranges and discussion of that.