Fat Tailed Thoughts: Stock Trading is Broken

Hey friends -

Welcome to the 8th issue of Fat Tailed Thoughts! We've been on a 22,579-word journey so far, or about 8.5% of the way to Ulysses. I hope you've been enjoying reading this weekly letter as much as I have been enjoying writing it. I really appreciate the encouragement and feedback as we've wandered from birds to blockchain, and from inflation to the internet. There's more to come!

In this week's letter:

Clearing & settling stock trades: 50 years of stagnation

Facts, figures, and links to keep you thinking over a drink

A drink to think it over

Total read time: 11 minutes, 19 seconds.

Stock trading infrastructure is broken

It's a provocative statement. And let's be realistic, our systems work pretty well most of the time for $140 trillion in stock trading done every year. The problem is that "pretty well" and "most of the time" aren't good enough. Would you invest your life's savings if you thought your trades might fail? Me neither.

This story isn't about the pretty screens that show stock prices bouncing around and new business models like no-fee stock brokerages. It's a dive into the heart of the system, the plumbing that transfers stocks from sellers to buyers and money from buyers to sellers.

Our story starts in the late 1960s when a paperwork crisis overwhelmed the world of the stock trading and hundreds of millions of dollars of stocks were stolen by organized crime. From the chaos emerged a new system in the early 1970s that's unchanged in its essentials through to today. While the system was innovative for its time, trading volumes have increased over 100x and the infrastructure is creaking under the load. We'll travel back to the present to understand how the system works - and sometime fails - today before looking towards the future where new technology already starting to transform the industry.

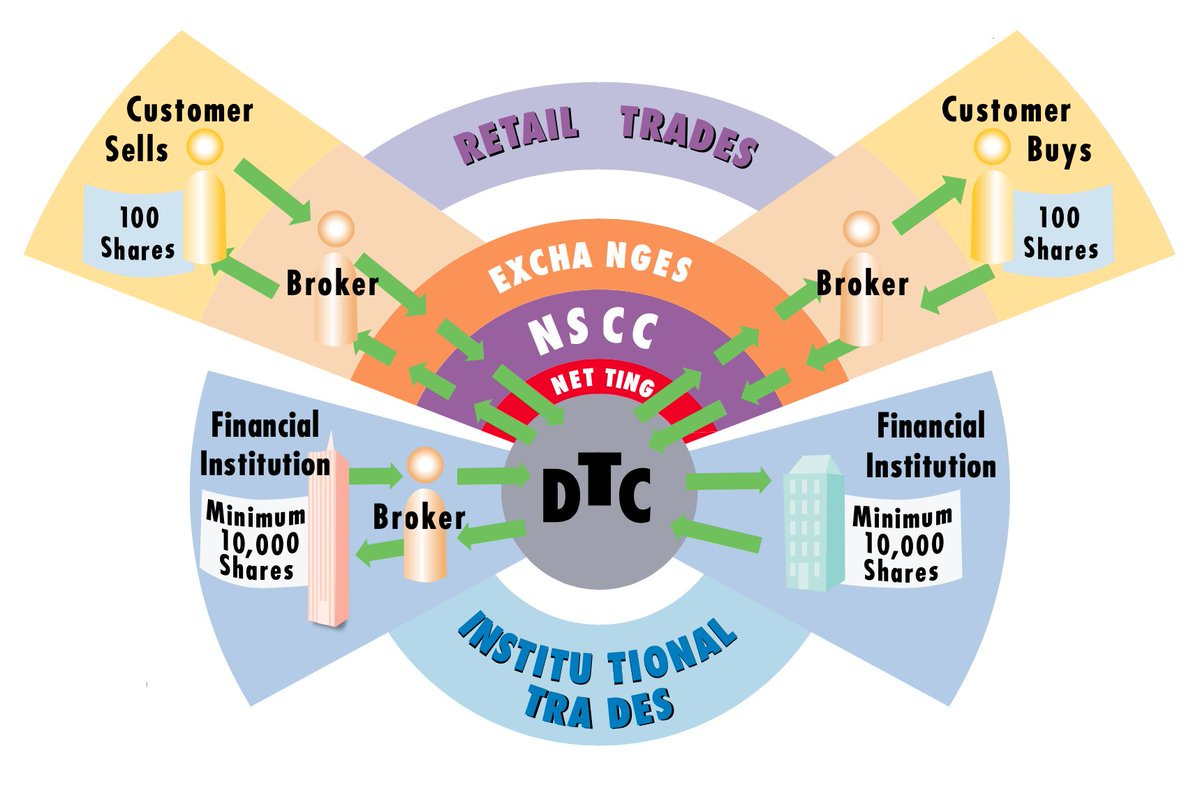

Important to keep in mind during the story is that individual buyers and sellers like you and me don't typically trade directly with one another. We use financial institutions that take our buy and sell orders, engage with each other, and then send us the results. The electronic trading systems we individuals use have seen lots of innovation. The stuff those financial institutions use, deep in the bowels of the system? Well, not so much.

The 1960s Paperwork Crisis

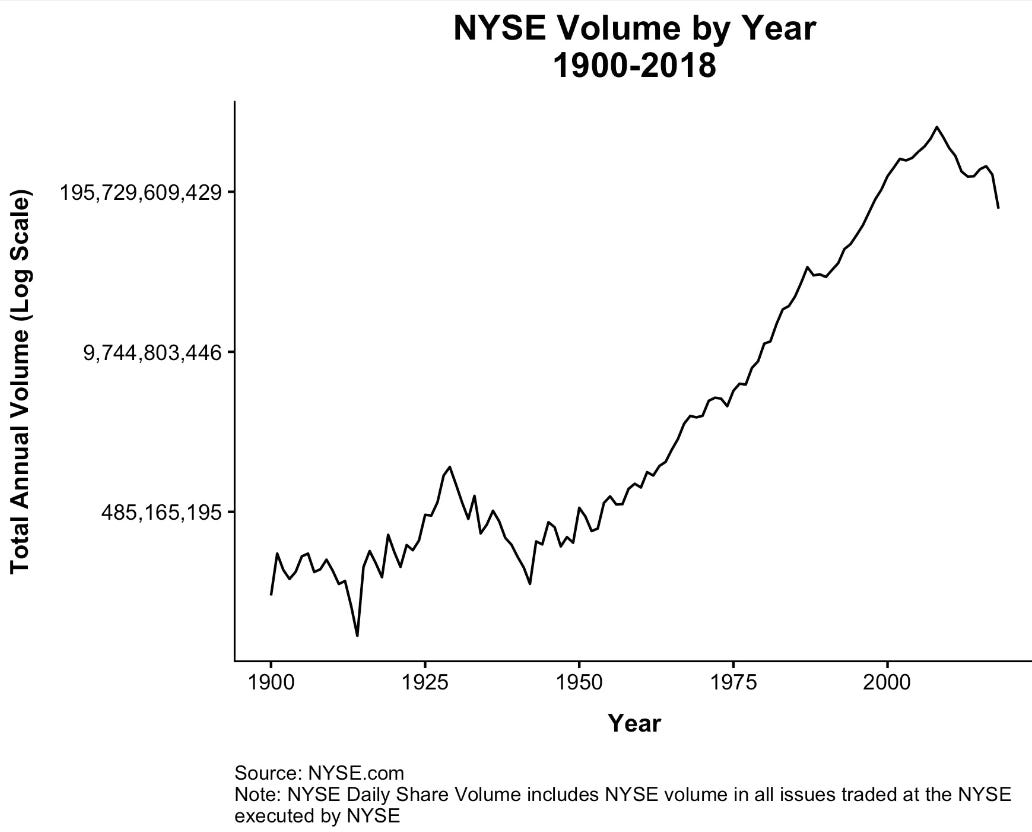

The 1960s on Wall Street were the Go-Go Years, replete with leisurely three-martini lunches in bespoke suits to break up the 10am - 3:30pm market hours. As the 60s wore on, mutual funds became all the rage and mom & pop investors piled into the stock market. Average daily trading increased 4x in just 6 years, from 3.8 million shares in 1962 to 14.9 million by 1968.

When a buyer wants to buy and a seller wants to sell, people and processes sit in between to make it happen. In the 60s, investors would phone or fax their orders to brokers and brokers would pass the order on to the floor traders at the exchanges. Floor traders would yell out the price and match up with someone on the other side of the trade to exchange handwritten orders. After a couple of different handoffs, the orders would eventually land in the back office. The back office then was every bit as glum as it sounds - a bunch of people, in a back office, dealing with paperwork.

The back office was responsible for clearing and settling the trade. Clearing is the process by which a seller's stuff is transferred to the buyer and the buyer's money is transferred to the seller. We say a trade is settled once clearing is completed. In the 1960s, clearing meant physically transferring paper-based stock certificates that served as bearer assets - whoever owned the certificate, owned the stock.

Financial institutions settled most trades bilaterally in the 60s, one-on-one between each pair of institutions without an intermediary. Because the stock certificates had to be exchanged, they did gross settlement. Gross settlement is in contrast to net settlement, which is more complex but results in fewer transactions.

Let’s take an example to understand gross versus net settlement. Let’s say you and I are doing business one day and I sell you 6 apples and you sell me 4 apples. If we’re doing doing gross settlement, then we’ll exchange all 10 apples back and forth. If instead we’re doing net settlement, I send you just the net 2 apples at the end of the day (6 minus 4). It requires more math and requires a time lag to build up trades that can be netted out, but it results in fewer actual transfers.

These inefficiencies posed by paper-based certificates and gross bilateral settlement meant that it took 5 days from the moment the traders agreed to buy/sell to the moment the certificate/money was exchanged. Even with t+5 settlement (trade + 5 days), the growing trading volumes overwhelmed the back offices. From the SEC's 1969 report:

Total complaints... jumped from 3,991 in fiscal 1968 to 12,494 in fiscal 1969... [F]or every letter of complaint sent to the Commission, 20 others are handled directly by the broker-dealer. Nine out of every 10 complaints currently filed relate to back-office matters... Accompanying the trading volume peak in December 1968 was a record number of 'fails to deliver' (securities contracts which a broker has not consummated by delivery of securities on settlement date).

In the sanitized language of a regulator, this is damning. The SEC was stating that not was the back office trigging huge volumes of complaints, the thing they were supposed to be doing - settling trades - wasn’t even happening!

The birth of centralized services

Short-term fixes, including switching to a 4 day trading week to allow the back office to catch up, failed to fix the problems. Congress hauled just about everyone to Washington, DC for hearings to identify a fix.

The hearings unearthed a troubling story beyond the fails to deliver - the US Attorney General estimated that over $400 million in stocks were stolen by organized crime during the settlement process, almost $3 billion in 2021 dollars. There wasn’t anything sophisticated about these crimes, criminals were simply pocketing the stock certificates and walking out the door. A fundamental rethink of clearing and settlement was needed.

Change came hard and fast in the early 1970s. The Depository Trust Company (DTC) was formed in 1973 as a central securities depository, owned by the very financial firms that needed to use it. That meant no more passing around paper certificates and instead, investors could reference stocks held at DTC. The National Securities Clearing Corporation (NSCC) followed shortly thereafter in 1976 to enable multilateral net settlement. Over 98% of trades today net out - meaning only 2% of trades result in financial firms exchanging stocks and cash on behalf of their investors.

DTC and NSCC have continued to innovate since their founding and were combined into a single entity - Depository Trust & Clearing Corporation (DTCC) - in 1999. Netting has gotten more sophisticated, many other services have been rolled out that help financial firms communicate with one another, and trade settlement times have been cut down to t+2 - two days from the buyer/seller agreeing to when payment and stocks are exchanged. Nonetheless, there were fundamental flaws in the original model that continue through to today.

Sowing the seeds for failure

The full costs of DTCC's new risks and complexity would only be fully realized in time, but the risks themselves become readily apparent with a quick look into how the firms actually work. The NCSS acts as a single central counterparty to trades - it is the buyer for every seller and is the seller for every buyer. This model ensures that even if the seller or buyer goes bankrupt, the trade can still go through. Once NSCC completes the trade, it sends settlement instructions (where to send what to whom) to financial firms facilitating the buy/sell orders and DTC communicates the net amounts of stock and payment to be exchanged. Payment is then routed through Fedwire, a system operated by the Federal Reserve exclusively for financial institutions to transfer money to one another.

This setup lays bear three major faults:

NCSS is a central counterparty - what happens if it goes bankrupt?

We can require firms to keep money at NCSS in case of bankruptcy, but who calculates how much money?

Payment is done separate from the exchange of stocks - how do we ensure that both stocks and payment are actually delivered?

We've found workarounds for all three problems, but they're expensive and don't always work. We mitigate bankruptcy risk in three ways: by having strict standards of who can use the NSCC services, by making NSCC member-owned to incentivize good behavior, and by requiring the financial institutions who use NCSS to put up margin. Margin is money that can be seized in the event of bankruptcy or similar failures. Similar to how the bank can seize your house if you fail to pay your mortgage, the financial institutions conducting trades through NCSS hold cash at NCSS that can be seized if they fail to pay or deliver the stocks.

We mitigate payment risk by executing the cash leg of the transaction first - the buyer doesn't officially take ownership of the stocks until they've delivered payment to the seller. We've replaced the risk of the seller transferring their stocks but not receiving payment with the risk that the stock sale doesn't happen at all.

When these workarounds fail, they tend to fail big.

Your margin account is $3 billion short, could you fix that by morning?

The bankruptcy risk fix shortcomings were realized on September 15, 2008, when Lehman Brothers unexpectedly declared bankruptcy. It took DTC and NCSS a full 6 weeks to untangle the $500 billion in trades that failed. This meant that there was at least that much capital tied up at NCSS and likely many multiples as investors had used the cash and stocks - now frozen - as collateral for loans. The problem was exacerbated as surviving NSCC participants were required to put up more margin as a backstop against other bankruptcies, ironically increasing the likelihood that one of those firms would now be short on cash. The risk of a single centralized party was realized at the worst possible time when the system could least tolerate it.

The margin requirement shortcomings can rear their head even without bankruptcy as we saw recently with GameStop. Robinhood is one of those financial institutions that engages directly with NCSS. Earlier this year, trading volumes in GameStop increased dramatically and chaos ensued.

If you're a financial institution that chooses NSCC to clear trades - and there's no major alternative available - you live with NCSS unilaterally determining how much cash you must hold at NSCC as margin. While daily margin requirements are predictable when markets are stable, the calculations themselves are a blackbox, and firms are only notified at 7am EST of new requirements that must be met in the subsequent 24 hours. You might be able to guess what happens when markets aren't stable.

With GameStop trading increasing, Robinhood received a 7am notice from NSCC that required them to put up $3 billion in new capital, an amount greater than the total capital they raised since its founding. Robinhood froze new GameStop buy orders, reducing the risk to NSCC in the event of a Robinhood bankruptcy, and the amount was reduced to $1.4 billion. Almost unbelievably, Robinhood was able to raise $1 billion overnight to meet the original demand and $2.4 billion in the following week to put the company back on firmer footing.

Who picked up the bill in the meantime? You and me. Many Robinhood users who traded GameStop using options found that their holdings were auto-sold on their behalf. Options are a financial derivative that gives you the right to buy/sell the stock at a predetermined price without purchasing the stock itself. Other users who borrowed money to purchase the GameStock stock found that they were overnight required to put up many multiples more money as margin to secure their loans. And while Robinhood's problems were exposing the shortcomings of margin requirements at NSCC, $359 million of GameStop trades simply failed to deliver (either the cash or the shared didn't show up) exposing the risks of separating payment into a separate system.

Where do we go from here?

The sources of DTC's and NSCC's problems are only growing in size. Daily stock trading volume continues to accelerate. It took 20 years to go from averaging 3.8 million shares a day in 1962 to a single 100 million share day in 1982, but just 6 years to double volumes from 2 billion to 4 billion between 2001 and 2007. This has been driven by both institutional investors like pension funds and everyday people like you and me. Not only has the US population grown over that time, but the percentage of people owning stocks also grew from 4.2% in 1950 to over 50% by 2010.

Technology and business model changes have similarly facilitated more and faster trading. Trades are now sent digitally and high-frequency trading firms often lay their own fiber optic cables to eke out ever-smaller speed advantages. Stocks pricing switched over from fractions to decimals in 2001 allowing more fine-grained prices to be submitted. "No-fee" stock brokerage firms like Robinhood encourage much more trading than has happened previously with fee-based trades. And all of this flows through infrastructure never designed for these loads and speeds.

For the first time in almost 50 years, new infrastructure is truly underway from both the incumbents and newcomers. DTCC released a proposal in February to shorten the settlement time from t+2 to t+1 by 2023. By their own estimates, shortening the settlement time "could bring a 41% reduction in the volatility component of NSCC’s margin." Integrating payments directly as part of the process, rather than having it done separately, is given consideration for a 2025-ish timeline. Perhaps unsurprisingly, the very same proposal advocates against moving to t+0 and other approaches such as real-time gross settlement due to a grab-bag of risks and required process changes.

A conservative view of DTCC's approach to change recognizes that they are critical infrastructure to processing stock trades that works pretty well most of the time, and that not-rocking-the-boat needs to be the first priority. A cynical view of DTCC's reluctance to adopt more radical changes sooner considers that their role as critical infrastructure will be materially reduced if the changes are implemented.

Paxos, a blockchain-based startup, is already piloting a clearing and settlement system that can facilitate t+0 with an integrated settlement capability that ensures both the stocks and payment go through successfully or the trade is canceled. The system is furthermore backward compatible, meaning that it supports the current t+2 settlement time, and flexible enough to support both netting and gross settlement. By executing gross settlement at t+0 and integrating payments, firms could choose to settle all trades in real-time and effectively eliminate bankruptcy risk.

Paxos isn't piloting these innovations as a wild outsider avoiding regulatory scrutiny. Instead, they've worked within the system as a regulated entity that's already integrated with DTCC. By participating as a good actor in the existing system, Paxos is likely to drive real innovation of the current system on a much more rapid timeline that pulls along DTCC at a faster clip than it may have moved in isolation. Joining the system as a regulated entity is a much harder path to take than the alternatives, but promises to create meaningful long-lasting changes that transform the world of stock clearing and settlement for the first time in 50 years.

Updating our stock clearing and settlement infrastructure is critical if we’re going to maintain trust in the system while supporting ever-increasing trade volumes. For the past 70 years, our stock markets have played a major role in increasing wealth for everyday people. As stock ownership increased from 5% of the population to over 50%, more and more ordinary people gained access to average returns of 7%+ a year, a rate that can double wealth every 10 years.

Failed trades and bankruptcies that reverberate across firms threaten individuals’ trust in the system, trust that is so critical to participation. New infrastructure should be put into production with a measure of caution appropriate for a system that handles trillions of dollars a day in trades, but that caution can’t stymie the changes that are clearly necessary. If the stock market is going to continue to play a major role in raising the living standards for the majority of the country, then we’re going to have to improve how we clear and settle trades.

Cocktail Talk

The COVID Delta variant continues to be front page news due to its ultrafast spread. Why does it spread so quickly? Early research indicates that infected individuals have 1000x+ the viral loads compared to those infected with the original strain and the incubation period is as much as 30% shorter.

An oldie but a goodie making the rounds recently - an account of Peter the Great’s beard tax in an effort to Europeanize Russia.

A third perspective on the never ending debate on the benefits and destruction of “progress.” Neither optimistic nor pessimistic, Jason Crawford argues for solutionism - problems are real, but solvable. (Thanks Trevor for the link!)

I recently finished Jim McKelvey’s Innovation Stack. It’s both the origin story of Square and very different take on entrepreneurship. You’ll find no false hope in 3-step-plans here. This the nitty gritty details and grind of a company succeeding against remarkable odds and the repeatable approach that can help others do the same. Dave Burkus’ “where there’s mystery, there’s margin” is apropos of the lessons here.

Your Weekly Cocktail

We're taking a detour from the fruity rum-based tiki drinks this week. It's all booze and it's all good!

La Rosita

1.5oz Espolon Reposado Tequila

0.5oz Campari

0.5oz Dolin Sweet Vermouth

0.5oz Dolin Dry Vermouth

1 dash Angostura Bitters

Grapefruit Peel

Pour everything into a mixing glass. Fill with ice until the ice comes over the top of the liquid. Stir ~50 times, about 20 seconds, until the outside of the glass is frosty. Pour into a rocks glass with ice, top with a grapefruit peel, and enjoy!

I don't quite know where to begin with this drink. It's kind of like Negroni (gin, sweet vermouth, Campari in equal proportions) but the tequila plays such a bigger role than the gin ever has. It's kind of like a perfect Manhattan (rye, sweet vermouth, dry vermouth, Angostura bitters) but the Campari takes us on a wildly different ride that the grapefruit peel accentuates. I dunno where Gary Regan came up with this, but you'll hear no complaints here. Well suited to the hot weather, this one's a bit unusual and I like it that way.

Cheers,

Jared