Fat Tailed Thoughts: The Money Supply

Hey friends -

We're continuing our dive into money, building off last week's letter that explored what is money. This week, we'll look into the money supply - how much money is there and how has that changed over time.

In this week's letter:

The money supply

The changing nature of venture capital, a dive into the much-beloved Wawa, and other cocktail talk

A cocktail that gets Better & Better

Total read time: 9 minutes, 58 seconds.

So. Much. Money.

Most of us don’t spend much time thinking about what money is, let alone how much of it exists. Yet while most of us might not be thinking about it, a remarkable experiment has been playing out over decades.

We’re printing money. A lot of money.

This isn’t money that’s constrained by the supply of gold or some other restraint, its money that can be created at will by central banks worldwide with few hinderances.

This is part of what Warren Buffett has called the Great Experiment and what his business partner Charlie Munger has aptly described as “nobody knows how much of this money printing we can do.”

We have ways of measuring all this central bank money, aptly called the money supply. The Federal Reserve, the US Central Bank, defines the money supply as:

the total amount of money—cash, coins, and balances in bank accounts—in circulation.

Not perfect, but we'll give it a pass for the moment.

The Fed continues with three ways to measure the money supply:

The monetary base: the sum of currency in circulation and reserve balances.

M1: the sum of currency held by the public and transaction deposits at depository institutions.

M2: M1 plus savings deposits, small-denomination time deposits, and retail money market mutual fund shares.

It’s a start. We’ll challenge these measurements in the future but for now we’ll engage.

Interlude - Recap of What is Money

A quick recap of last week's letter as this week's letter assumes you're familiar with the definition of money.

Money is not just one thing, it varies both in its uses and attributes. Different monies optimize for different attributes to be a better fit for different uses.

Money has three primary uses:

It’s a store of value, meaning that money allows you to defer consumption until a later date.

It’s a unit of account, meaning that it allows you to assign a value to different goods without having to compare them. So instead of saying that a Rolex watch is worth six cows, you can just say it costs $10,000.

And it’s a medium of exchange—an easy and efficient way for you and me and others to trade goods and services with one another.

Money can have five major attributes:

Universally accessible - the degree to which it is easy to obtain and use

Electronic - money can be dematerialized or physical

Centrally issued - the degree of centralization of the issuing authority

Peer-to-peer - money can be exchanged directly between individuals or go through intermediaries

Supply-constrained - the degree to which creation of money is constrained or not

Back to this week's letter.

How to Measure Money Supply

The Fed's money supply definition and measurements are restricted to dollars and dollar-linked instruments. If a competing money were to emerge in the US, the Fed's definitions would exclude it.

The Fed's money supply can be more accurately renamed the US dollar supply. By extension, the European Central Bank's money supply can be renamed the euro supply, and the Bank of Japan's the yen supply. We'll collectively call these and other central bank-based measurements of the money supply, central bank money supplies.

While it does not account for all monies, central bank money is the majority of money in circulation. It's worthwhile to start by looking at their supplies before we branch out.

Measuring Central Bank Money Supplies

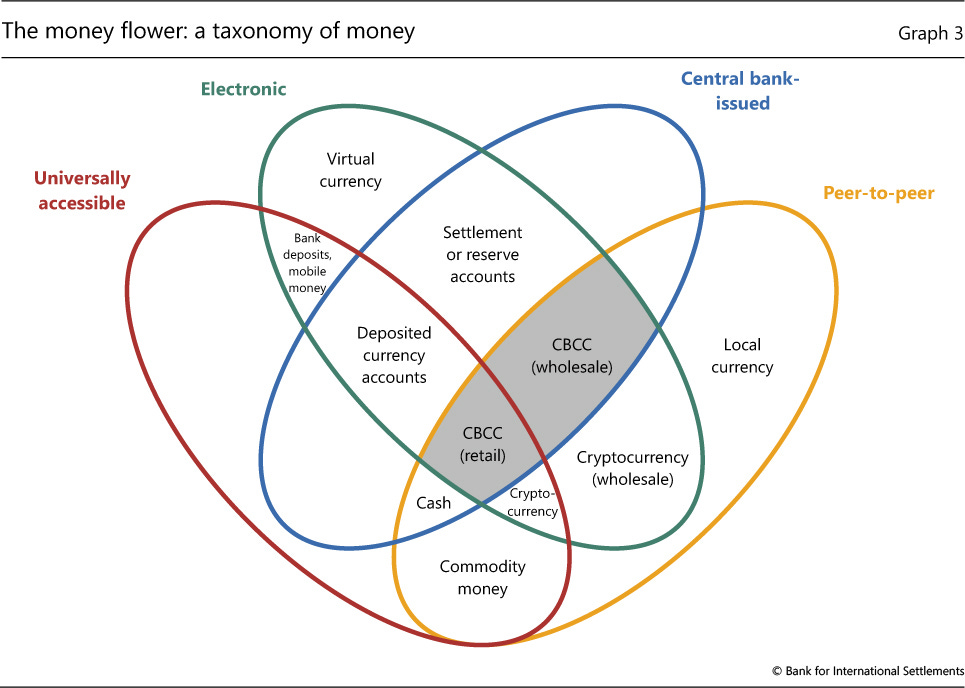

We'll use the central banks' own measurements to look at how the central bank money supplies have changed over time. The Money Flower from last week can help us categorize the different types of central bank monies.

The monetary base is an effective measurement for the most liquid central bank monies. It includes the currency in circulation - what's labeled cash in the diagram - as well as deposits that banks hold at the central bank, similar to how you might have a checking account at your bank. These central bank deposits are known as reserve balances.

Note that while both of these monies are central bank-issued, they differ in all other respects. Cash is physical, universally accessible, and exchanged peer-to-peer whereas reserve balances are electronic and restricted to banks permitted to hold deposits at the central bank. As a result, these two monies can behave very differently despite being lumped together.

M1 is another measure of the money supply. It includes the monetary base and some less liquid central bank monies, mostly made up of checking accounts, savings accounts, and other types of transaction deposits held at banks. In the diagram, these transaction deposits are lumped into bank deposits. M1 critically does not include mobile money, even when based on central bank monies. This excludes over $2 billion in daily transactional volume executed by 121 million mobile money holders in Africa.

M2 is an even broader measure that includes even less liquid instruments. It includes M1, money market accounts, money market funds, and certificates of deposit (CDs) less than $100,000.

Interestingly, BIS's Money Flower does not consider money market accounts and funds as types of money. They're a good example of something that is money-like but may or may not be money. Money market vehicles hold most of their investments in cash or short-term treasury bills and commercial paper that can rapidly be converted to cash. The problem is that when the financial markets panic and almost no one will buy anything - such as what happened to the Reserve Primary Fund in 2008 - it becomes readily apparent that money market funds are not cash equivalents. Unlike an FDIC-insured bank account, there's also no guarantee of getting your money back. This makes it a worse store of value than bank deposits.

Nonetheless, you can do many of the same things with a money market account that you can with bank deposits - you can write checks, wire money from an account, and withdraw money at will. That's roughly comparable to bank deposits as a medium of exchange. Money-like, but may or may not truly be money.

There are two more measurements of money, M3 and M4, that track increasingly illiquid assets such as T-Bills (US federal government-issued debt that matures in less than a year). While some other central banks continue to publish measurements of M3 and M4, the US does not. For this reason and because we're already on the edge of what actually meets the definition of money with money markets, we're going to ignore M3 and M4 measurements.

It's worth noting that these measurement definitions are specific to the US and vary slightly as we go across other countries. For the sake of simplicity, we'll express non-dollar central bank monies using the measurement definitions above.

Central Bank Money Supplies

Let's take a look at the three largest freely traded currencies - the US dollar, the Euro, and the Yen. We're leaving the Chinese Yuan out of the comparison because it is not freely traded in the same sense as the other currencies and the data is unreliable.

US Dollar Supply

The story of the US monetary base is straightforward - slow and steady growth until the Great Recession, then an unprecedented expansion in the money supply. Whereas it took 23 years from 1995 to 2008 for the monetary base to double, it took just a few short months between August and December 2008 for it to double again. We added another $1.7 trillion to the monetary base in the first three months of the pandemic, an amount greater than the entire monetary base in December 2008.

We can see how the Fed handled the last two crises by splitting out the reserve balances - money held by banks at the Fed. This was a tool that was rarely used before 2008 and is clearly now in vogue. Since July 2008, reserve balances have increased 240x.

By including checking accounts, savings accounts, and the like, M1 shows just how dramatic the recent pandemic-related intervention truly was (note that this chart switched to billions). M1 balloons from $4 trillion to $16 trillion in a handful of months. It has steadily climbed upwards ever since adding another $3 trillion since June 2020. To frame this - after the immediate pandemic relief, we added additional money to the economy equivalent to 75% of all M2 dollars that existed in February 2020.

It's not until we look at M2 that we start to see a more muted effect. The major change here is that M2 accounts for money in money market accounts and funds. These are often the next best cash equivalents when you're above the $250,000 limit for FDIC insurance on a bank account, a hurdle that moves us out of individuals' savings and into businesses. The pandemic safety net was largely targeted at individuals so we see a more muted effect on the dollar supply as we branch out to include how businesses hold money.

Even with the more muted effect, the growth is nonetheless dramatic. The money supply roughly doubled every 10-15 years from 1975 through 2020.

The conclusion from the US dollar supply is straightforward yet shocking. The interventions in 2008 were unprecedented... until 2020. We took the 2008 playbook to such an extreme that money could not be absorbed as cash and bank reserves so it flowed to bank deposits instead. This was done against a backdrop of existing money supply growth for almost 50 years. We've never tried anything of the like before and it's anyone's guess how this will play out.

Euro Money Supply

Europe's M1 mostly only tracks the amount of currency in circulation, so it's not particularly helpful as a comparison point. Europe's M2 reasonably approximates the US's M1 for our purposes so we'll start here. A note on reading the graph: units are millions of euros.

The money supply growth isn't very dramatic compared to the US - a steady uptick over time with a small pandemic-related jump. Other related measures tell a similar story. Dig a little deeper and we see that the money supply doubles between 1990 and 2000, and then doubles again by 2010. Growth has decelerated slightly - the supply looks like it'll take until at least 2025 to double again.

What we have is clearly a different way of dealing with crises, one that doesn't involve creating a massive new euro supply.

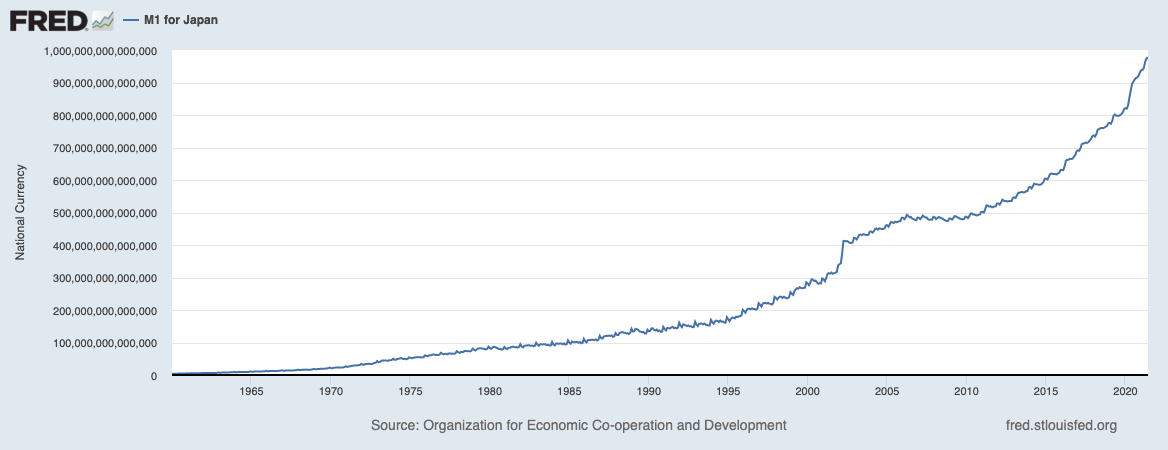

Yen Money Supply

Japan doesn't formally track the monetary base, so we'll start by looking at M1 which includes currency and bank deposits. Japan tells a very different story than the US or Europe. The supply of M1 yen doubled in the 10 years between 1975 and 1985 and then doubled again by the end of 1995. It doubles yet again in the next 7 years before the growth rate levels off. In the 27 years between 1975 and 2002, the money supply grew 8x from ¥50 trillion to over ¥400 trillion. M2 and other measures tell a similar story.

Here we can trace an experience that is more akin to Europe than the US. Japan's money supply steadily doubled on a roughly 10-year cycle starting in 1975, but we don't see nearly the dramatic jumps that the US sees in response to crises.

Money Printer Go Brrrrrrrr

It's evident most major countries have been pursuing a money printing agenda for almost 50 years. While 2008 and the recent pandemic resulted in an unprecedented new supply of US dollars, it's nonetheless a continuation of the longer-term trend.

What's remarkable is that these accounts don't consider the competing monies that have emerged since the dawn of the digital age. Take another look at that Money Flower. We haven't even begun measuring virtual currency, mobile money, cryptocurrency, and many other types of money. You can imagine that these are enormous sandboxes for those who want to experiment with reinventing money.

What if we want a money that exists digitally, is universally accessible, and isn't subject to a centralized issuer? That's not available with central bank money. What if we want a money whose value is based on some commodity so the supply tracks the supply of the commodity? Also not available with central bank money.

Digital, and more recently blockchain, have given us a whole new toolkit to invent new kinds of money. This has been going on far longer than the recent attention given to bitcoin. It's where we're headed next week - the other monies supply.

Cocktail Talk

Venture capital has gone through a revolution in the past decade, marked by ever-increasing round sizes and the professionalization of early stages. Longtime venture capitalist Mark Suster dives into how the industry has changed and how that has affected his firm in his recent blog post. (Both Sides of the Table)

Tweet thread diving into the much-loved Wawa. $10B in revenue, 35K employees, and still a privately owned family affair. (Twitter)

In a continued theme of eroding digital freedoms, both Apple and Google kowtowed to Russian government pressure to remove Kremlin critic Navalny's app from the respective app stores ahead of the Russian presidential "election." Telegram, a secure messaging app, followed suit shortly thereafter. (Reuters)

In sad news, Norm MacDonald, a giant in the world of comedy, passed away after a protracted battle with cancer. An alumnus of Saturday Night Live and a regular on the talk show circuit, his style of comedy was unlike any other seen before or since. You can catch a glimpse with his moth joke on Conan and his rather colorful interpretation of Burt Reynolds on SNL's Celebrity Jeopardy.

Your Weekly Cocktail

Evenings are starting to have that ever-so-slight cold nip in the air. New weather means new cocktails!

Better & Better

1.5oz Del Maguey Vida Mezcal

0.5oz Smith & Cross Traditional Pot Still Rum

0.25oz Velvet Falernum

Pour all of the ingredients into a mixing glass. Add ice until it comes over the top of the liquor. Stir until the outside of the glass is frosty, ~20 seconds. Strain into a rocks glass filled with ice. Enjoy slowly while contemplating what fall will bring.

This drink's a nice crossover as we protest saying goodbye to summer and embrace fall. The first couple sips pack a punch - Vida mezcal is a heavy hitter and the pot still rum is overproof. The falernum serves as the sweetener and rounds out some of the alcohol tones. This is a drink - as the name suggests - best enjoyed over time. As the ice melts and the alcohol level falls, the drink transforms to bring out a mellow smokiness from the mezcal and spiced sweetness from the rum. It does a great job exemplifying how a liquor or a cocktail can change dramatically as the alcohol content varies. You might even say this one gets Better & Better.

Cheers,

Jared