Fat Tailed Thoughts: What is Money?

Hey friends -

We're going to embark on a big topic - money. We live in a remarkable time where anonymous software engineers can create novel "internet money" worth over $1 trillion and where the technology that underpins that innovation forces central banks to revisit the foundations of money as we know it today.

To critically analyze what's happening today with money, we first have to understand what money is. From there we can look at how the money supply has grown over time before looking at the remarkable work underway today to create new and different forms of money. Special thanks to Steve Dickens and Sachin for suggesting the topic!

This is too big a topic to do justice in a single letter. For today, we'll focus on what money is.

In this week's letter:

What is money?

Potty-trained cows, an Ig Nobel prize for discovering that the obesity of a country's politicians may be a good indicator of that country's corruption, and other cocktail talk

The Pineapple Daiquiri, a great drink in a pointless glass

Total read time: 10 minutes, 12 seconds.

Money makes the world go round

Many years ago I had a wonderful history teacher who peppered lessons with songs from opera and movies, sung with full gusto. I can comfortably picture him now in front of a class of teenagers, dancing on his desk and singing:

Money makes the world go around

...the world go around

...the world go around.

Money makes the world go around

It makes the world go 'round.

A mark, a yen, a buck or a pound

...a buck or a pound

...a buck or a pound.

Is all that makes the world go around

That clinking, clanking sound...

Can make the world go 'round.

Despite what I'm sure were the film writers' best efforts, the story of money is a bit bigger than just that which makes "that clinking, clanking sound." Stuff that clinks and clanks is but one type of money - there's a whole lot more.

What is money?

Let's start with why money exists. It has three primary uses:

It’s a store of value, meaning that money allows you to defer consumption until a later date.

It’s a unit of account, meaning that it allows you to assign a value to different goods without having to compare them. So instead of saying that a Rolex watch is worth six cows, you can just say it costs $10,000.

And it’s a medium of exchange—an easy and efficient way for you and me and others to trade goods and services with one another.

If we look at some of the earliest forms of money, we find mediums that serve some-but-not-all of these uses. Tally sticks and clay tablets served as useful monies of account as far back as 5000 BCE in Mesopotamia, tracking debts owed for taxes and other transactions. Clay tokens in Mesopotamia and wampum in the United States served as monies of exchange to facilitate trade.

The first monies already took on two of the four forms of money we'll eventually explore: representative money and commodity money. Representative money is a medium of exchange that has little-to-no intrinsic value itself, but instead represents a claim on some underlying good. For instance, the clay tokens of Mesopotamia represented transferable claims on grains stored in a warehouse. Commodity money is the opposite - it has intrinsic value and is used for exchange, such as wampum used for jewelry and payment.

Commodity and representative monies were the only forms of money for most of human history, most notably including those clicking clanking coins made from precious metals. They facilitated remarkable innovation including bills of exchange for trade, demand deposits such as checking accounts, and many others. But at its core, the issuance of all these monies was constrained by the volume and availability of the underlying commodity on which the money was based whether that be precious metals or trussed ducks.

That changed in the 11th century when China pioneered the third form of money - fiat money - represented as a paper banknote. Fiat money is money issued by a central government authority declared to be legal tender that cannot be converted at a fixed value to a commodity. Fiat money didn't really take hold globally until the 1900s with the United States notably abandoning the dollar-to-gold peg in 1971. We are now in the midst of experimenting with a new fourth form of money - cryptocurrency - that shares the attributes of fiat money but is not issued by a central authority.

What we need is a way to compare not just money's uses but also its attributes so we can start to make sense of all of these different forms.

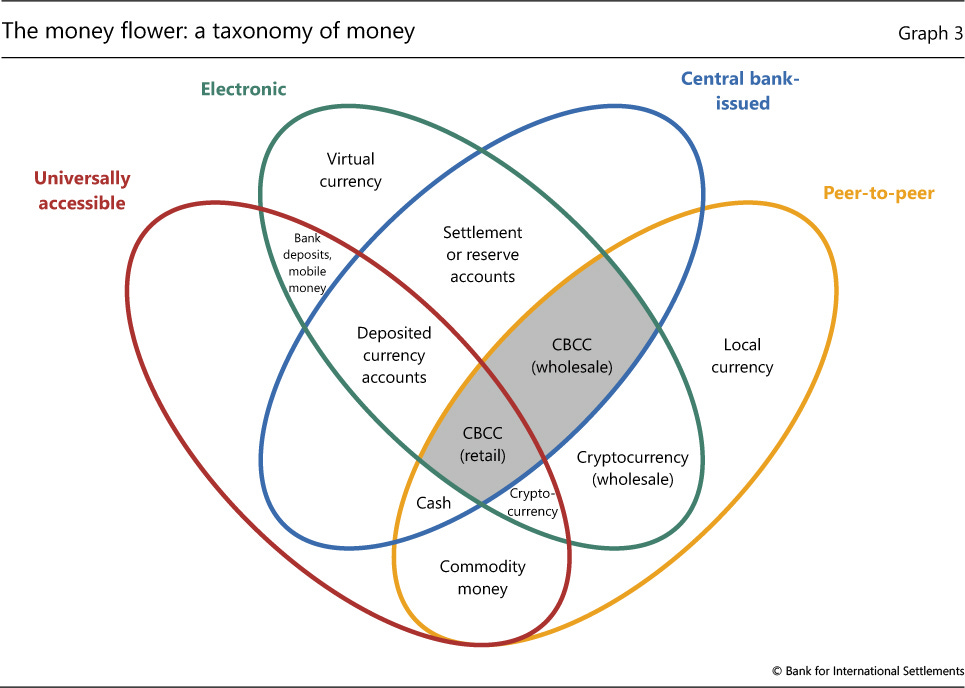

The Money Flower

The Bank for International Settlements (BIS) felt the same way. A bit of context on BIS - if a central bank like the Federal Reserve in the United States is the bank for a country's banks, then BIS is the bank for central banks. They're the oldest and among the most prominent international financial institutions and recently they too have been grappling with the recent emergence of a new form of money. To frame the discussion and compare attributes across forms of money, they came up with the Money Flower in 2017.

Not only is the Money Flower visually attractive, it remarkably captures almost all of the key attributes in an easily consumable diagram. Supply constrained is the only major attribute that's missing. Let's go through each of these attributes in turn.

Universally Accessible

Universally accessible money is easy to obtain and use. There's an ongoing debate if that concept is analogous to anonymity, the degree to which a third party or central administrator can track identity and transaction details.

Cash and coins are fully anonymous and accessible to all by being physical bearer assets, where bearer means that possession is ownership. Especially in countries without rule-of-law or with governments who have a habit of confiscating property, these are hugely important attributes. They meaningfully hinder attempts to confiscate wealth. The tradeoff is that it can incentivize theft precisely because ownership is near impossible to track.

I challenge BIS’s categorization of bank deposits and deposited currency accounts (individuals' bank deposits at the central bank, a not widely used model) as universally accessible. Over 20% of the world's population lacks access to banking services and those numbers are well over 60% for the majority of Africa. Even cash isn’t fully accessible. We've instituted laws to make cash less accessible over time, including in the US that you can't take out more than $10,000 in cash from ATMs in a day.

The conflict between accessibility and anonymity does not come from an overt desire to reduce accessibility, it comes from a desire to reduce anonymity - we want to track (and hinder) individuals who attempt to use dollars to fund terrorists and drug trafficking. Most cryptocurrencies strike a pseudonymous balance - a public record of transactions linked to anonymous accounts. At least to date, we haven't found a way to make fully accessible money that isn't anonymous, suggesting that the attributes are two sides of the same coin.

Electronic

We can think of electronic as the physicality of the money - is the money dematerialized or physical. Most of what we encounter is dematerialized, whether that be savings accounts or Venmo accounts.

We find electronic money is also highly prevalent throughout the $150+ billion video game industry, such as PokéCoin used to purchase goods in Pokemon Go and V-Bucks used to purchase goods in Fortnite. These are not small universes - over $5 billion was spent in V-Bucks in 2020 alone, 10 times bigger than Tonga’s GDP. Why the comparsion? Tonga has its own fiat currency, the Tongan pa’anga. The “Fortnite economy” is 10x that of Tonga.

Central Bank Issued

I take issue with the phrasing here. If we modify this to centrally issued, meaning it is created by a central authority, then we have a workable definition. Case in point - cash issued in 11th century China predates Henry Thornton's concept for a central bank by about 700 years. I'll give BIS a pass on this one - they're owned by 63 central banks and anything other than "central bank issued" probably wasn't going to make it through the editing process.

Centrally issued is the key long-term problem with most monies. While the life of a currency is certainly longer than the now-debunked 27 years bitcoin enthusiasts proclaim, the temptation to debase the money - reduce its value - is often too great for struggling central powers to ignore. In modern times we see this with the $100 trillion notes from Zimbabwe ($250 for four bills on eBay), no different than in the past when cheaper metals were used to reduce the purity of coins. The seemingly inevitable outcome is for the currency to become defunct.

Monies not issued by central authorities have different challenges. Take commodity money for example. Rapid increases and shortages of the underlying commodity can have dramatic near-term effects on the money supply leading to rapid episodes of inflation and deflation. Especially in a pre-digital world where information traveled more slowly, knowledge of a boom or shortage could give individuals asymmetric advantages as to the value of the commodity money. Such asymmetries undermine everyones' trust in the money's value.

Peer-to-Peer

Peer-to-peer is the degree to which money ownership can be transferred without a central intermediary. Cash and other physical bearer monies are at a far end of the spectrum and require no intermediary whatsoever - I can give the physical bearer monies to you and now they're yours.

Electronic monies require some form of intermediary, typically a server to which the senders and receivers both connect. With the innovation of cryptocurrency, we can decentralize that intermediary such that with enough independent servers working in tandem the system becomes peer-to-peer.

While helpful, blockchains are not strictly necessarily for a peer-to-peer electronic money to exist. Riksbank, the central bank of Sweden, is exploring the viability of the e-krona as a proposed peer-to-peer electronic equivalent to cash that would still be issued by the central bank.

Supply-Constrained

This one I don’t excuse BIS for excluding. This is in theory the solution to the over-enthusiastic central money issuer - supply-constrained money that has either a finite quantity or an unchangeable growth rate. Perhaps unsurprising that a party owned by none-other-than central money issuers would have left this out.

Issuers of precious metal coins attempted to instill public faith in the supply constraint by maintaining published coinage purity. We already saw how that turned out in Rome. The ultimate challenge of using a commodity to limit the supply of money is that some party has to verify that the commodity-to-money ratio remains intact. That party is almost always centralized and abuses its position of power over time.

By being electronic and decentralized, cryptocurrencies can credibly constrain supply - supply limits can be embedded in code and no single party can alter the code. While that doesn't eliminate ways to devalue the currency, such as collusion to modify the code, it can meaningfully reduce the likelihood of such an occurrence. This is not a comment on whether credible supply constraint is good for money generally, but rather an acknowledgment that this is truly novel.

So Many Different Monies

What we originally set out to analyze - what money is - turns out to be more a concept than a clean definition. We use it as a store of value, unit of account, and medium of exchange. But as we found by looking at the different attributes, different monies trade-off among the three uses to suit specific needs.

Cash works great as a medium of exchange and unit of account, but its ability to store value is highly dependent on the trustworthiness of whichever central authority issued it. Central issuers have generally abysmal track records over long periods.

Bank deposits can be more reliable stores of value by paying interest to offset devaluation, but they're not at all useful as a medium of exchange or unit of account (imagine if you had to pay for everything with a check). We've solved for both through complex clearing and settlement systems like credit cards, but that just further diminishes the accessibility of bank deposits - a card is just another hurdle for an unbanked person.

We can keep poking holes in all of the monies - settlement and reserves accounts are not useful units of account, local currencies by their very definition are not widely accessible, and virtual currencies such as PokéCoin are neither stores of value or units of account. This is precisely why we have many types of monies each of which is optimized to solve for some combination of the store of value, unit of account, and medium of exchange trifecta. That optimization necessarily makes tradeoffs among money's five attributes, tradeoffs that determine where the monies might be useful and how much trust money holders will have that the money will satisfy its intended use.

We'll keep exploring money next week by looking at how the money supply has changed over time. A fair warning - it'll likely get messy. Life would be much easier if we just looked at cash, but as we've seen, we have to include many different types of monies if we want a deeper understanding of what's actually going on.

Cocktail Talk

You've probably heard of the Nobel Prize, but have you heard of the Ig Nobels? Awarded every year since 1991 for "achievements that first make people laugh, and then make them think," previous awards include a 2020 Medicine Prize for diagnosing long-unrecognized medical condition - misophonia - the distress at hearing other people make chewing sounds and a 2019 Physics Prize for determining how wombats make cube-shaped poo. Check out this year's 2021 winners awarded last week. (Ars Technica)

One very determined group of scientists has potty-trained cows. More than just bathroom humor, bovine waste is both a major source of greenhouse gas and poses significant health risks to the cows themselves. Proper loo etiquette could help with both. (Science)

Gas too expensive? Don't blame the gas station owner, they're probably just as upset as you are. They're making money from the convenience store and the air machine, not the gas. It's a business model that's almost 70 years old. Check out The Hustle for a deep dive. (The Hustle)

Apropos of our exploration of money, Brazil is running into some problems with its new real-time payment system. It works so well that "lightning kidnappings" are up 40% since it launched. (Finextra via JP Koning)

Your Weekly Cocktail

Holding on to summer with at least one more fruity cocktail!

Pineapple Daiquiri

1.0oz Plantation Stiggins' Fancy Pineapple Rum

1.0oz Plantation 3 Star White Rum

1.5oz Pineapple Juice

0.5oz Lime Juice

0.5oz Coconut Sugar Syrup

Despite a love of gin, I've never really been a martini person. In part, because there are so many other cocktails that are far more exciting, but mostly because I never quite learned how to drink out of a martini glass without sloshing it all over myself. Even with all my misgivings, I figured a martini glass was needed to do this one justice. It’s a fun drink - it looks refined, but it’s a tiki drink at heart.

The lime makes the drink more pineapple-y than it would be alone and the acidity of both the juices tames the sweetness of the rum. And what a rum it is. I highly recommend getting a bottle of the pineapple rum, a revived 1824 recipe made by infusing the rinds from Victoria Pineapples into the 3 Star rum for a drink that's equally at home in a cocktail or on the rocks.

For the record - both the rum and the cocktail taste even better in a rocks glass, especially because they'll make it into your mouth rather than your lap.

Cheers,

Jared