Fat Tailed Thoughts: Crypto Market Size

Hey friends -

Over the past few weeks, I've had some fun conversations around how big crypto is. A challenge for me continues to contextual - how big is crypto relative to other stuff whose value grew incredibly fast?

In this week's letter:

Crypto - how big is it really and how does that compare to the growth of other assets?

Facts, figures, and links to keep you thinking over a drink

A drink to think it over

Total read time: 8 minutes, 0 seconds.

Growth Benchmarked

If you spend even a short in time in the cryptocurrency world, you will inevitably come across a statement like Pomp's:

The "fastest growing... in history." That's a big claim. It also comes with a lot of baggage including - critically - how do you measure growth?

(If you need an intro or refresher on cryptocurrencies before venturing further, checkout my earlier notes: crypto intro, crypto market overview.)

One way to measure crypto’s growth would be to look at the number of people that own crypto. Gemini, a cryptocurrency company and exchange, estimates that 21.2 million US adults - about 14% of the population - own crypto today, 12 years after the launch of Bitcoin. That's a pittance at internet scale. Even back in 1993, Marc Andreessen and the team at Netscape scaled the Mosaic web browser to over 1 million users in the first year. TikTok has over 1 billion users and its not even 5 years old. User growth is not likely to be the place to look.

A better way to measure crypto’s growth is based on dollar-denominated value, otherwise known as market capitalization. Scaling that value by GDP will allow us to measure how impactful the development of crypto was relative to the time it happened. For context, we'll look at three big historic booms in US history - oil, gold, and the 1990s stock market - before we look at the still ongoing crypto boom.

Oil

Oil in the US has an incredible history, starting first as whale-fat-alternative kerosene for illumination before being repurposed for gasoline, diesel, and all variety of related energy sources.

Oil was first discovered in large quantities in Pennsylvania in 1859. Like many good US origin stories, this led to a massive wave of hype and innovation followed by the almost inevitable over-investment, over-production, and price collapse. From the ashes rose John D. Rockefeller's Standard Oil in 1870, not as a producer but as a refiner and marketing company to create a "more orderly" market.

With oil fever on the mind of the public and improvements in geology, oil was subsequently discovered elsewhere through Appalachia during the late 1800s leading to small but steady increases in production almost every year. Yet more oil was discovered in Kansas and then again in Oklahoma in the late 1890s giving hope to those, including Rockefeller, who feared that oil might be a geographically scarce resource.

Texas - today known as the biggest oil-producing state - didn't show up on the scene until 1901. When it finally showed up, it did it in a Texas-sized way - a gusher of oil shooting over 50 feet into the sky.

With oil playing such a major role in our country's history and geopolitics, I expected the value of crude oil production to be a meaningful percentage of GDP. Not so.

The value of crude oil produced in any given year peaked at around 3% of GDP during the late 70s oil crisis. For most of history, the value is closer to 1.5% of GDP. This is a lesson that Rockefeller learned early on - Standard Oil left the drilling to others and instead made much higher margins on refining and selling it.

The year-over-year change in value as a percentage of GDP reinforces a similar story.

This graph is the slope of the value as a % of GDP (the orange line) from the previous graph. Anything over 0% is growth and larger numbers demonstrate more rapid change. Extended positive and negative periods, such as the negative stretch from 1950 to 1970, are longer term year-over-year trends.

The slowly declining trendline reflects the continued decline of oil production as a meaningful component of our economy. Critical to note here is that oil is consumed. It has little chance to accumulate so the value is dependent on the annual production and the then prevailing price. Gold, however, is forever.

Gold

Gold needs no introduction and only minimal background. It has been a store of value and medium of exchange across cultures and throughout history, and we have reasonably reliable prices for gold going back to 1257 in Britain. Most of the world's gold is not consumed for utilitarian purposes, but rather makes its way into jewelry, bullion, and pop culture.

Gold production in the US predates the California gold rush by nearly 50 years. Gold was first found in Virginia in 1804. While never particularly productive, mining in Virginia continued through until the Civil War and then resumed again in marginal capacity until the eve of World War II.

The US saw a series of minor gold rushes in Georgia (1829), Alabama (1830), and elsewhere in advance of the annexation of California and the subsequent California Gold Rush in 1848. Contrary to popular belief, this was by no means the peak of US gold production but rather a prelude to almost 100 years of significant production.

As a percentage of global gold production, the US peaked during the California Gold Rush and has been giving up market share consistently since the late 1800s. Value as a percentage of GDP follows a similar path with some notable exceptions.

Unlike oil, the value of gold as a percent of GDP skyrockets to over 15% in the boom times of the 1849 Gold Rush. That relative value stays elevated through the entirety of the Civil War before it starts a long-term relative decline. The three other peaks we see are times of major fear - the 1929 stock market crash, the inflation debacle of the late 70s, and the financial crisis of 2008.

The year-over-year change in value as a percentage of GDP gives greater insight into the two different types of events.

You can see that the value percentage changes persist much longer in the case of new supply in 1849 than they do in the case of price shocks such as in the late '70s. This is in large part because the government maintained a fixed purchase price for gold that did not vary with supply. So unlike oil where the market reacted to new oil supplies by reducing price and thus value for that period, the total value of gold was free to appreciate irrespective of supply booms. For extended periods when there was a gold rush, this meant that the total value of gold could steadily increase relative to GDP, such as the unabated growth period from the California Gold Rush in 1848 to the eve of the Civil War in 1861. Nonetheless, as GDP continues to grow faster than gold production, the long-term trend is for the value of gold to be a smaller and smaller percentage of GDP.

Gold isn't consumed, it persists over time. So too do public companies but, unlike gold, there is no floor price so the total value is free to fluctuate with regulatory change, fear, and other exogenous events.

Stocks

The stock market is almost as old as the country. The New York Stock Exchange started in 1792, two years after the first exchange formed in Philadelphia. The dominance of the New York Stock Exchange was slow to start but accelerated rapidly after the telegraph broadened access to the exchange and reduced the need for regional players.

The basics of the exchange continue through to today and it remains the largest stock exchange in the world - over $25 trillion of public company shares are listed on the exchange. While in recent years the stock market has made its way into popular culture, that wasn't always the case. Even throughout most of the 1900s, the stock market was only a fraction of the relative size it is today.

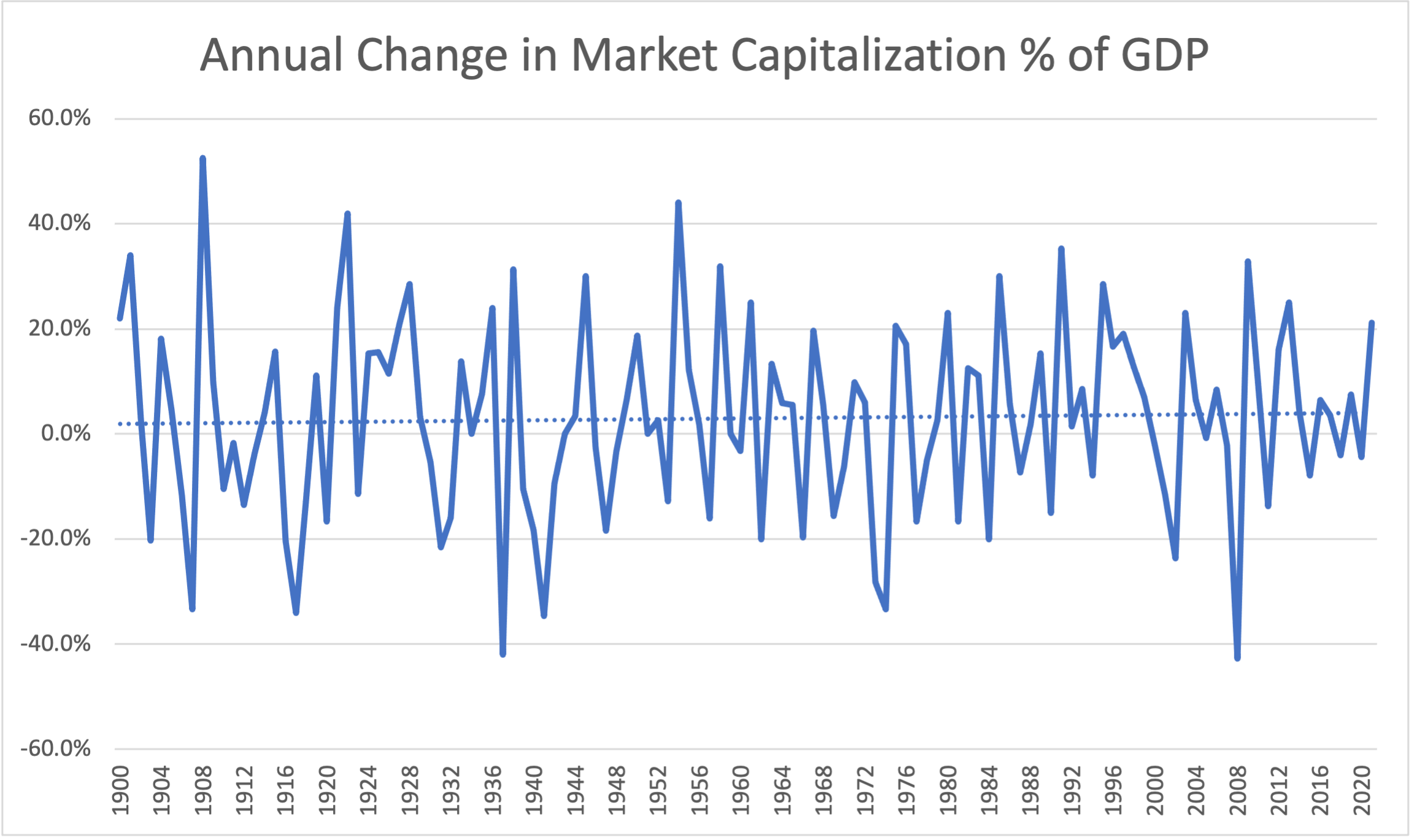

Even in the roaring '20s and the Go-Go '60s, the stock market remained smaller than GDP. It wasn't until the tech boom of the '90s that we saw the overall value of the market really take off. It was the two bookend periods - the '20s and the '90s - where we see persistent growth as a percentage of GDP.

From 1924 until the crash in 1929, the stock market more than doubles its relative size versus GDP. The '90s boom interestingly starts at 90% of GDP - almost identical to the peak in 1929 - before growing to 151% of GDP before the crash in 2000. While a smaller relative increase, the 90s nonetheless stand out.

With oil, gold, and stocks as context, let's dive into crypto.

Crypto

Our dataset is necessary smaller - Bitcoin only launched in 2008 and reliable price data dates to 2009. While Bitcoin remains the dominant cryptocurrency, others have emerged over time including Ethereum in 2015. Bitcoin nonetheless retained 80%+ market dominance until the 2017 crypto boom.

To build a full dataset back to 2008, I've used the Bitcoin market cap through mid-2013 and the CoinMarketCap dataset for subsequent periods. I took quarterly samples in each annual period to account for the impact of price volatility, a methodology that appears to be directionally informative.

The scale of crypto is remarkable. From too small to matter in 2016, the total value of crypto is now almost 7% of GDP. The growth is apparent when we look at the year-over-year change in value compared to GDP.

The short version of this chart is that the numbers simply don't fit. Look at the scale on the left. Numbers that would be remarkable in almost any other context - 86% growth in 2018 - look almost trivial here. Although difficult to view, total market capitalization actually declined by 36% and 28% in 2015 and 2019 respectively, but it hardly registers here against the magnitude of the growth. This is crazy.

Comparing Growth

Even among assets famous for booms of tremendous growth, crypto stands in a league of its own. While small relative to the stock market, in just 12 years it has twice as large relative to GDP than oil ever achieved and almost half of what gold achieved in the wake of the 1849 gold rush.

In terms of relative annual change, nothing comes close to crypto. Even if we dismiss the early years of growth because crypto was small relative to GDP, the growth in 2017 is almost 10x the next largest relative growth rate, that of oil in 1865 as soldiers returned home from the Civil War hoping to strike it rich.

I didn't set out to prove Pomp's claim that crypto is the fastest-growing financial asset of all time and yet the data is incontrovertible. Among the assets in the history of the US economy that have been meaningfully large relative to GDP, crypto is in a league of its own.

Cocktail Talk

The amazing story behind Trader Joe's $2 wine, Two Buck Chuck. How Fred Franzia (yes, that Franzia!) turned a $27,000 brand into a $100+ million a year machine. (The Hustle)

A great dive into multifactor authentication - why you have to type in a username, password, and a code sent to your phone. It's a security approach that relies on what you know (password) and what you have (phone). (Patryk's blog)

Why are hyperlinks blue? (Mozilla)

Female jacobin hummingbirds have evolved to look almost identical to their flashy male counterparts. The reason? Males harass drably-dressed females but leave the flashy ones to feed in peace. (The Atlantic)

Your Weekly Cocktail

One invented by yours truly this week!

Sunset Point

2.0oz Dark Rum

1.0oz Aperol

2.0oz Grapefruit

1.0oz Lime

1.0oz Brown Sugar Syrup

1 dash Angostura Bitters

Pour all of the ingredients into a shaker. Fill with ice until the alcohol is covered. Shake for ~20 seconds, until the outside of the shaker is frosty. Fill a rocks glass with ice and strain the drink into the rocks glass. Find yourself someplace poolside or on the water and enjoy!

Necessity is the mother of invention. I was spending time with family and we all wanted something grapefruity and rum-based. My repertoire of rum + grapefruit drinks until this was practically nonexistent. This drink marries the grapefruit bitterness of Aperol with the caramel of rum and brown sugar. Lime helps intensify the grapefruit and Angostura the same for baking spices notes in rum. We ended up making two batches of these (ran out of ice the second time) and I doubt they'll be the last!

Cheers,

Jared