Fat Tailed Thoughts: The Slow Revolutions in Financial Services

Much of what's hyped today will take years to mature. What's the state of yesterday's hype?

Hey friends -

A thought struck me as we recorded our top 10 predictions for 2022 - a lot of what's hyped today will take years to mature into the mainstream.

Take the internet boom for instance. Most of the 20/20 hindsight focuses on the craziness of the late 90s, but most of the companies we engage with today weren't even started then. Google was founded in 1998 but didn’t make a real splash until it becomes the default search engine for Yahoo! in 2000. Facebook was founded in 2004. Netflix starts streaming video in 2007. The giants we know today happened in the 2000s after the internet had become commonplace, not in the 90s when it was front-page news.

That's all consumer-facing. Businesses innovate more slowly and regulated businesses more slowly even still.

What was hyped yesterday and is only just starting to transform financial services today?

In this week's letter:

A quiet revolution in financial services: rebuilding critical infrastructure for the next 50 years

Facts, figures, and links to keep you thinking over a drink

A drink to think it over

Total read time: 14 minutes, 20 seconds.

A Seismic Shift Underway

There's a company missing from that "internet boom" list - or rather, a subsidiary. Amazon Web Services (AWS), the first Cloud computing platform. It launched in 2002.

As consumers, we interact with cloud-based computer services every day. Gmail? Cloud. Turbotax? Cloud. Pretty much every app on your phone? Also cloud. Think of the cloud as someone else's computer - rather than owning lots of expensive hardware yourself, you rent a little bit of hardware from a cloud provider and only pay for what you use. That allows you to have a lightweight device like a phone and offload the heavy lifting - like storing lots of cat videos - to the cloud provider.

Cloud is now a massive business. AWS alone generates over $64 billion in sales per year and is growing at over 30% a year. And they're just one-third of the market!

Despite this massive adoption over the two decades since cloud launched, financial services has only just begun to adopt cloud. Only 8% of banking technology workloads have moved to the cloud. That leaves 92% still to go!

And yet, all of the innovations that we're going to explore are built on this shift to the cloud.

What's so special about the cloud?

The implications of switching from owning hardware to building in the cloud is a topic large enough to fill many letters. Three key changes have been essential to the transformations underway today in financial services.

1. Specialization

Financial services companies are in the business of finance. That may include some technology, such as developing a new mobile banking or stock trading application for customers. They're not in the business of databases, networking, and all of the other behind-the-scenes technologies.

Cloud enables companies to outsource the behind-the-scenes technology to specialists like AWS. The specialists deliver the technology as shared services across all of the clients they support, allowing the specialists to build once and deliver many times. That's a recipe for rapid improvements.

What does that mean for the financial services companies? Not only do they transfer the headache of managing technology to the cloud specialist, but they also end up with a much higher quality product! The result is that financial services companies increasingly outsource non-core technology to specialists, creating a massive opportunity for more specialist technology companies.

2. Narrowed focus

Not all of the technology is outsourced to the cloud provider. Some of it stays within the financial services company or is bought from technology companies and run on the cloud.

Which technologies do the financial services companies keep? The ones that are part of their core competencies, including customer-facing apps, underwriting modeling for loans, and risk models.

The narrowed focus means that the financial services companies themselves are also building faster and better products!

3. Externalized services

This remains the biggest hurdle to further cloud adoption by financial services companies. It was a brand new muscle for the companies to develop and one that continues to take work developing today.

When you own your own data center, you limit the frequency with which you share data outside of the company. All of the data sharing happens through applications that you also develop and own.

When you move to the cloud, you store your data and trade secrets in someone else's data center! All day, every day you share data outside of the company. That means you have to build security protocols, processes, and interfaces so you can do so safely and seamlessly.

That new muscle - sharing data externally - accelerates the rate at which financial services companies can integrate technologies from third parties. Deciding how to share data with each new third-party technology vendor isn't a one-off activity that has to be rethought and managed as a novel project. Instead, managing data sharing with third parties becomes a core competency!

Together, specialization, a narrowed focus, and externalized services have unlocked a much faster pace of innovation for traditional financial services companies. It's starting to bear fruit.

Reinventing Capital Markets

There's a revolution happening in capital markets. While LendingClub, Robinhood, and other startups have made headlines as new consumer-facing applications for borrowing and stock trading, slower but more substantial changes are happening under the surface.

The core plumbing that allows stocks and debt to be issued, traded, and settled is undergoing transformation for the first time in decades. This isn't like replacing a tire while the car's still running - it's like swapping the engine out.

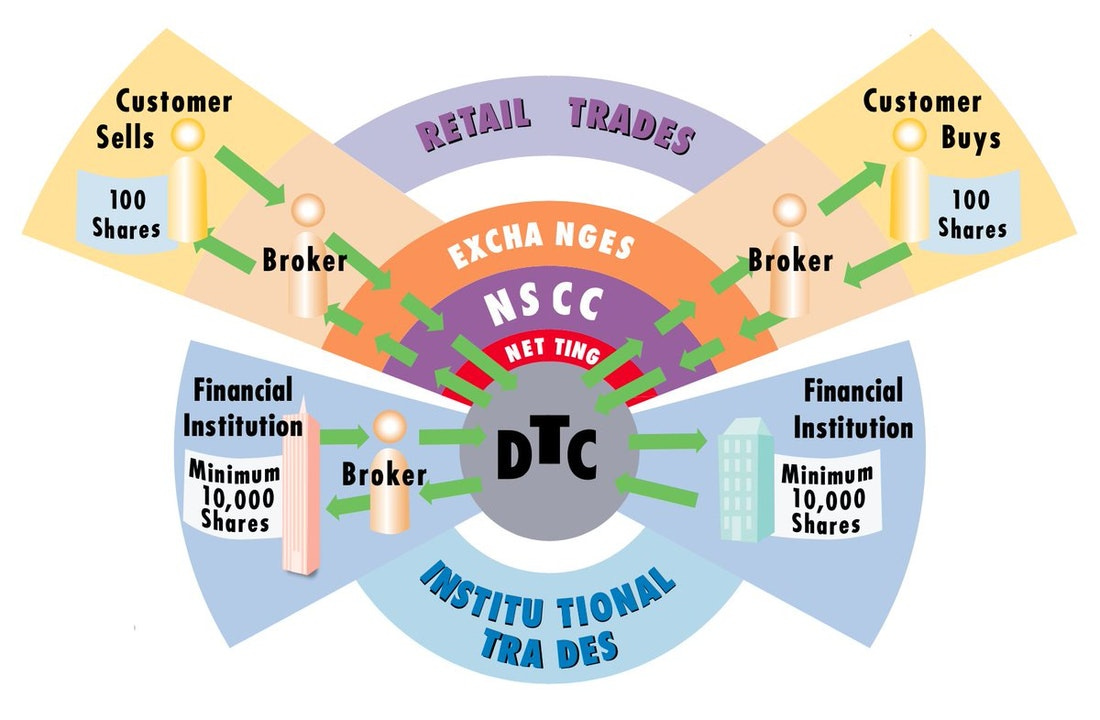

Settling stock trades

When you buy or sell stocks, your order is relayed through a complex network of intermediaries the net effect of which is to transfer shares from seller to buyer and money from buyer to seller. At the core of this system sits Depository Trust & Clearing Corporation, DTCC. It's massive - an average day in 2020 saw over $1.75 trillion flow through their systems.

I previously wrote about the full story of how DTCC came to be and the challenges it faces today as stock trading volumes have continued on an ever-upwards trend. There are three major problems alongside a whole host of smaller ones:

DTCC is the single central counterparty to all trades. After a lot of intermediaries and steps, the buyer or seller on the other side of the trade is replaced with DTCC. That shields you from the risk that you deliver your half of the trade - shares or money - and the other party goes bankrupt before they deliver their half. But the solution introduces the new risk that DTCC goes bankrupt.

DTCC requires the financial services companies that use their services put up margin - money - in case they go bankrupt and can't make good on their customers' trades. Margin calculations are blackbox and can blindside companies when market conditions are abnormal. A recent example includes the plight of Robinhood. When meme-stock Gamestop saw unusually high trading volumes, Robinhood received a 7am notice from DTCC that they needed to put up an additional $3 billion in margin within the next 24 hours or effectively have their business shut down. That was more than the total amount of money Robinhood had raised up to that point.

DTCC processes the movement of stocks separately from the movement of money. That makes it very difficult to disentangle trades when something goes wrong, like when Lehman Brothers went bankrupt in 2008. Over $500 billion in trades failed. It took 6 weeks to untangle the mess and tied up money many companies needed to fix losses related to the bankruptcy.

We've built workarounds for all three problems and many of the smaller ones. But they're just that - workarounds. The margin requirement (#2) was a workaround to bankruptcy risk (#1), but it's now clear the solution simply traded one problem for another.

But a revolution is underway.

DTCC itself is already at the forefront. Together with other major industry players, they have proposed transitioning from a 2-day settlement time to a 1-day settlement time. This would mean that the shares and money are exchanged one day after a trade matches.1 Work is already underway to prepare the many changes necessary to support such a shift, but the magnitude is such that it won't go into effect until 2024 at the earliest.

DTCC has also been piloting Project Ion, a blockchain-based settlement system that would allow for same-day settlement and more tightly couple the movement of stocks to the movement of money. That's on track to move into limited availability in the next couple of months.

But wait a second. Blockchain allows the two sides of the trade - buyer and seller - to exchange shares without any centralized intermediary and still have no bankruptcy risk. Why use DTCC at all?

Paxos has been settling stock trades on their platform since February 2020. They built a brand-new settlement service, built on blockchain, that is already settling trades same-day, next day, or 2-days at their clients' demand. It's the first time in decades that the industry has a viable alternative to DTCC. You can imagine the innovation an independent, profit-driven startup can bring to a process that's been monopolized by an industry-owned for over 50 years.

The only limiting factor is regulatory approval. Paxos applied for but does not yet have a full clearing agency license. They secured approval back in October 2019 to operate for a "Feasibility Study No-Action Phase" with up to seven financial services customers and a limited volume of stock trades.

That approval expires after two years by which time Paxos will likely have secured a clearing agency license. Everything to date indicates remarkable success. Last year, the company raised $300 million from investors including Bank of America, who also joined as a settlement service customer. ABN AMRO later joined as the sixth settlement service customer. These are among the major financial services companies facilitating stock trading today now piloting the technology of tomorrow with Paxos.

Come this time next year, financial services customers will have two new blockchain-based stock settlement services to choose from - one offered by incumbent DTCC and another by startup Paxos. That's a massive change from the 50-year status quo.

Not to be left behind, debt markets are undergoing their own revolution.

Digital & automated debt markets

Despite all the room for improvement, stock trading is nonetheless largely automated. Debt markets are not. They mostly run on paper and we've already seen the massive problems they creates. Even just the markets for debt issued by companies are massive - in the third quarter of 2021, over $200 billion was issued across 287 deals in Europe alone. That's a lot of paperwork.

Debt is more nuanced than stocks. The shares in most public companies are fungible - it doesn't matter which specific share you own. Debt is far more heterogeneous. A debt issuance by a company may include many different types of debt that pay different interest rates, mature in different years, and grant the holders different rights in bankruptcy.

Most of this data is trapped on paper. Warren Buffett famously estimated that if you wanted to fully understand a single CDO squared, a particularly complex debt-based asset, you'd have to read an accompanying 750,000 pages of terms specific to just that one asset! You can imagine that if you start with such a mess, many of the surrounding processes like facilitating interest payments on the debt are similarly manual.

A digital alternative is starting to emerge.

Singapore multinational bank DBS partnered with startup Nivaura for a first-of-a-kind digital and automated debt issuance and trading platform in Asia. For the first time, all of the data is digitized. Machine-readable data unlocks the ability to automate many currently manual processes. Debt issuers - companies - can connect directly with debt buyers without going through banks as intermediaries.

This isn't a pipe dream, it's live. Keppel Corporation was the debut issuer earlier this year with a €1 billion debt issuance.

Europe isn't letting Asia get too far ahead. In September, SIX Digital Exchange secured regulatory approval for a new digital bond exchange and then issued the initial debt with three Swiss banks.

In just 6 months, we went from a fully paper-based market to two live, fully digital bond markets.

Stocks and debt are just half the equation. What about the money used to pay for them?

Reinventing Money Movement

Money isn’t just currency, it includes many different types of money. The measure of how much money exists is the money supply. The monetary base is the most restrictive measure of the money supply. It includes currency in circulation and reserve balances at the central bank. M2 is a broader measure of money supply that includes both the monetary base and other types of money including those created by private bank lending and money markets.

The monetary base is just 30% of M2. A full 70% of the money supply is created by private financial services companies! And that's a relatively low percentage historically. In August 2008, just before the massive Financial Crisis related stimulus packages, the monetary base was just 10% of M2!

You can learn more about the money supply from the previous letter.

Reserve balances and those other moneys aren't physical like a dollar or a coin - they're recorded as IOUs on ledgers maintained by financial services companies. Elon Musk pithily summed up the state of money in a recent podcast:

Right now, the monetary system is a bunch of heterogenous mainframes running COBOL in batch mode.

If those terms aren't familiar, it's because you don't hear them much anymore. Mainframes were the "it" technology in the 1970s and are what powered IBM to its heights. COBOL is the programming language used on mainframes. Said more simply, most moneys other than physical currency live on 50+ year-old technology.

But that's changing.

Interbank money movement

While most TV pundits have been commentating on the price of Bitcoin and Congress has been hauling stablecoin issuers into hearings, two companies have quietly been facilitating billions of dollars across brand new payment networks.

If you've ever wondered how cryptocurrency companies convert their crypto to dollars, the answer probably involves startup Tassat. They built a blockchain-based interbank network where banks can create and exchange tokens that are fully backed by their customer deposits. Unlike existing interbank systems facilitated by the central bank or centralized clearinghouses, this one directly connects banks peer-to-peer. Money can move instantly, every minute, of every day.

Tassat's biggest customer today is New York's Signature Bank. A full 16% of deposits at Signature - totaling $10 billion - are from cryptocurrency customers. Many of these customers are cryptocurrency exchanges who want to make dollars instantly available to customers who wish to sell their crypto.

The startup has gone further than just selling their network to banks - they've integrated the network into most of the major core banking systems. Core banking systems are the beating heart of the most essential bank operators including deposits and lending. Anyone using one of the major vendors already integrated with Tassat, who collectively make up over 90% of the market, can seamlessly join the new payment network.

The vision of where this all goes is extremely compelling. Tassat recently raised $40 million to launch a new company - The Digital Interbank Network - and is contributing all of the intellectual property and related assets to the new entity. The new company will own and govern the payment network. And who is lined up to own the new company? The banks themselves! That's an extraordinarily strong incentive to make it a success.

Tassat is a technology company selling to banks. Alternatively, you could build a new payment network as a bank and encourage other banks to join. JP Morgan has been doing exactly that.

JP Morgan Coin Systems is currently used to enable bank customers to move funds among accounts at the bank. The roadmap is to facilitate money movement among banks globally, similar to what The Digital Interbank Network has already piloted domestically.

JP Morgan is already halfway there. Three sister products already enable banks on JP Morgan's network to send payment queries and instructions, like validating that the intended receiving account exists. As Coin Systems expands from just JP Morgan to the full network, the participants will be able to send the money too.

We're reinventing money for the first time in 50 years and banks already have two networks to choose from!

Reinventing Slowly Then Quickly

All of these awesome innovations - new infrastructure for stocks and bonds, new ways to move money, and more - are all playing out on decade-long horizons. Despite being slow moving, they’re wonderfully exciting.

Try to think back to a time pre-smartphone or pre-internet. We couldn’t imagine then what those foundational technologies would unlock and yet today we can barely imagine living without them.

These decade plus long financial services transformations are very much the same. They’re a reimagining of the most fundamental components of finance that all of us take for granted and few of us even know exist. They will become the foundation for new financial services we can’t even imagine.

It all begins with the innovations we’re watching unfold today.

Cocktail Talk

Watch the busiest subway system in the world, live. An enterprising software developer built a 3D visualization of the entire Tokyo subway system and hooked it up to live data feeds. You can do everything from tracking trains as they move along the tracks to watching it happen live through webcam feeds. All of this is possible because of Open Data initiatives in Japan. It's one of the coolest projects I've seen in some time. (Mini Tokyo 3D)

Is your car dealership still short on inventory? Blame the semiconductor shortage. Electronic systems account for over a third of the cost of a new car. Lots of electronics require lots of semiconductors, a trend that will continue as cars turn electric and incorporate ever more bells and whistles. That demand continues to massively outstrip supply and shows no sign of abating. (Fabricated Knowledge)

The US is falling behind on semiconductor production. We launched 50% fewer semiconductor fabrication projects in the past decade than we did the decade before. The time it takes each project to go from construction to production increased by 30%. We're not doing much and we're doing it slowly. The rest of the world has taken notice. China launched 4 times as many semiconductor fabrication projects and did so 25% faster per project. Even the island country of Taiwan launched more projects than the US and again 25% faster than the US. It's time to build. (Center for Security and Emerging Technology)

If you're in financial technology and don't know what the regulators do, you're like a one-legged man in an ass-kicking contest - good luck. This is the best overview of financial regulators I've ever read. It walks through the essentials - who the regulators are, what they do, how they interact with one another, and who regulates which activities. It also inadvertently exposes why navigating regulators in the US is such a difficult task. (Congressional Research Service)

Your Weekly Cocktail

New year, a new family of cocktails to explore.

Orange You Glad I Didn't Say Banana

0.75oz Bourbon

0.75oz Laird's Apple Brandy

0.25oz Drambuie

0.25oz Cointreau

2 dashes Orange Bitters

1 dash Ginger Bitters

Orange peel

Pour everything into a rocks glass. Squeeze the orange peel over the drink to express the oils and discard.

What's odd about this drink? There's no ice! It's a scaffa, a family of room temperature drinks made without dilution. Scaffas typically feature strong flavors from bitters or amari, that remarkably diverse family of Italian herbal liqueurs including Campari and Aperol. The lack of dilution or cold allows these flavors to shine more prominently than in traditional cocktails. This drink is no exception. It takes the apple-forward How Do I Compare from Sother Teague and transforms it into a spiced-orange variant that remains wonderfully drinkable despite the mix of high-proof-only components. It's so good that it has been increasingly finding its way into my regular rotation, the first scaffa to do so. It helps that you can make this ahead of time and store it, although mine never seems to last!

Cheers,

Jared

Lots more on how it all works here