Fat Tailed Thoughts: What If Debt Collectors Helped Rather Than Abused?

Technology is powering a new approach to debt collections - help rather than abuse. It not only makes consumers happier. It's better business.

Hey friends -

We're venturing into another financial services failure - debt collection. The industry remarkably couples high costs and low collection rates with a generally abusive customer experience. And yet it's essential to the functioning of financial services.

A handful of startups have realized there's an opportunity for innovation. It might not be sexy, but they're making a tremendous difference in millions of lives.

In this week's letter:

Debt collection: the beginnings of change in an industry where it's much overdue

PayPal is launching a stablecoin, fish are nesting like birds, and more cocktail talk

An unexpected revamp of the classic, the Toffee Negroni

Total read time: 16 minutes, 51 seconds.

A Recipe for Abuse

Debt collection is about as well set up for consumer abuse as any industry I've come across. It's baked into the fabric of how debt collection arises in the first place.

You purchase a good or service from a vendor. Rather than pay immediately, you agree to pay the vendor in the future. Then, you don't pay. Such a scenario could play out with a credit card - you fail to pay your credit card bill - or with a hospital where you don't pay your medical bill.

The vendor now has to choose how it will collect on the payment owed. There are four options:

Try to collect the money owed itself,

Outsource collections to a third-party collections agency,

Sell the debt to a debt buyer, or

Don't collect at all and write off the debt as a loss.

All three options where the debt is pursued for payment are ripe for abuse. Options two and three, where the collections are outsourced or the debt is sold, are particularly troublesome. The debtor has no relationship with the party trying to collect the debt. The party collecting the debt won't have a future relationship with the debtor.

Why bother treating the debtor well? Why not abuse them and see if you can collect more money?

A faulty premise

Abusing debtors has been the go-to solution for most of history. Debtors' prison was the primary way to deal with unpaid debts. The philosophy was that such punishment would encourage individuals to pay their debts.

Systematic abuse of debtors continues today. The industry is the #1 source of fraud complaints to the Federal Trade Commission and the #2 source of complaints to the Consumer Financial Protection Bureau (CFPB).

The reality is that most people want to pay their debts. Most delinquent debts - debts not yet paid past their due date - arise from mistakes or crises. Maybe you thought you canceled a monthly service and forgot to pay for the final month. Maybe you lost your job and couldn't make a car payment.

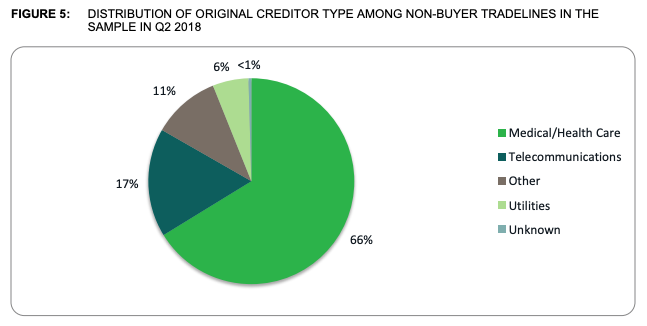

The breakdown of debt in collections in the US makes this abundantly clear. 66% of debt with collections agencies is from medical or healthcare.

Most of the medical bills that end up collections are from unexpected crises. Perhaps unsurprisingly, unexpected medical bills are also the leading cause of bankruptcy.

The vast majority of individuals with unpaid debts are and remain well-intentioned. They want to pay off their debts. They simply don't have the money right now.

Lots of Debt = Lots of Collections

It's hardly an exaggeration to state that the US is built on debt. Household debt is about three-quarters of GDP. Non-housing debt makes up about a third of that.

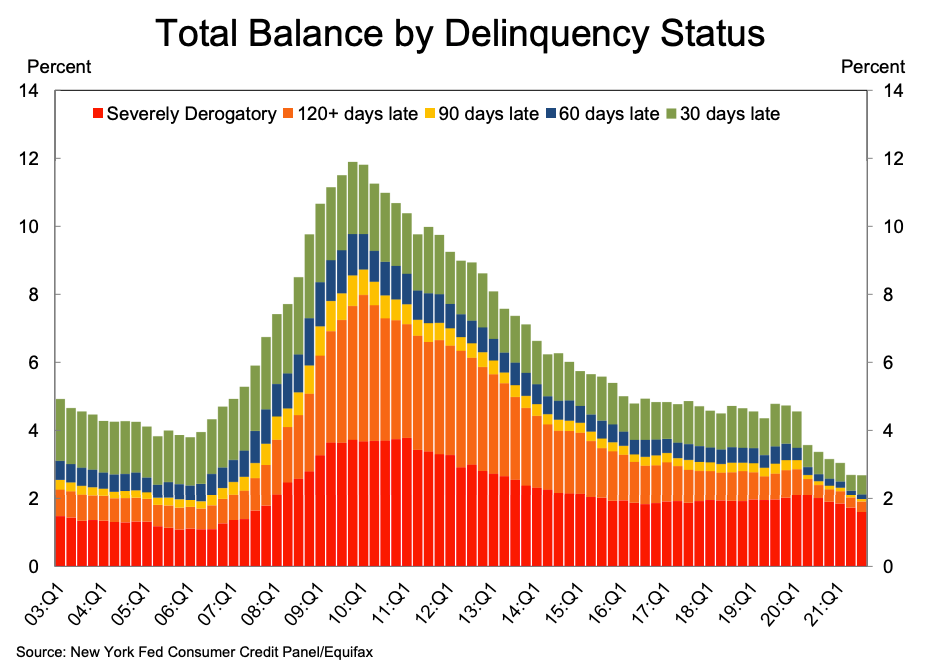

Not all of that debt gets paid or paid on time. Especially in times of turmoil, such as during The Great Recession, debt delinquencies can balloon.

Debt delinquency trends reinforce the premise that most people want to pay their debts but sometimes struggle to do so. Between 2-4% of debt balances are severely delinquent - more than 150 days late. That relatively stable subset makes up the majority of bad actors. The remaining delinquent debt balances, which make up 2-8% of total debt balances in any given period, fluctuate with overall macroeconomic conditions. Those are consumers trying to pay off their debts but are unable to do so right now.

Only about 10% of delinquent debt is sent to debt collections agencies or debt buyers. The majority is managed internally or written off. The higher liquidation rate for collections when kept internally - the percentage of outstanding money owed that is actually collected - is a major driver for keeping the debt rather than outsourcing.

That higher liquidation rate is offset by the costs of supporting an in-house collections team. By contrast, most third-party debt collection agencies operate on a contingency basis - they only get paid if they successfully collect the debt. The commission is a percentage of the recovered debt and typically starts at 20%. While 20% may seem high, it's more-than-justified by the $90 billion that was recovered by agencies in 2019 alone.

Managing debt collection agencies comes with its own costs, namely vendor risk management. An agency that fails to abide by regulations or the company's policies poses a significant liability. Most companies engage multiple agencies to mitigate such risks and keep commissions low. The average credit card issuer for instance works with seven agencies.

Working with multiple agencies also allows companies to try collecting a delinquent debt multiple times. For a specific debt, a given agency will try to collect the debt for a predefined period. If they fail to collect, the company can re-allocate that debt to a secondary agency. From there, they can reallocate again to tertiary and quaternary agencies. The liquidation rate falls off as the delinquent debts age and are passed among multiple agencies.

The system is structured to make it highly economical to try to recover many delinquencies, not just a small volume of large ones. The median debt in collections is just $366 and the average owed is only $1000. Medical is even smaller - the median is $207 and the average is $579. As a result, over 25% of all US consumers have at least one debt in collections as of 2018. It's a robust trend that only varies a couple of percentage points a year including during The Great Recession.

This steady population of "delinquent debt consumers" underpins collections industry growth during economic downturns. Rather than taking on larger debts, they tend to have more debts in collections. Even today, with relatively low volumes of debt in collections, the average consumer in debt owes money to four different lenders. The Great Recession is emblematic - volumes with agencies grew 75% between 2004 and 2013 and then declined to just above the 2004 starting point by 2018.

Taken as a whole, the debt collections industry demonstrates some fairly interesting dynamics:

Always large and often increasing US household ensures a steady supply of delinquent debt to service

A steady percentage of consumers with delinquent debt keeps the supply of consumers growing with the overall population, about 1% per year

Variable economic conditions create boom-and-bust opportunities for agencies as the number of delinquent debts per consumer follows the macroeconomic situation

The result is that the number of collections agencies and debt buyers tends to vary with macroeconomic conditions with an undercurrent towards consolidation. The numbers of agencies and buyers peaked in the years leading up to The Great Recession and have been on a steady decline ever since. As of 2018, the number of buyers was down 75% from the peak to 40, and the number of active agencies down 60% to 898.

Particularly troubling is that these trends reinforce the likelihood of consumer abuse. Fly-by-night operations can make money in the boom times and disappear before their antics are uncovered. Fewer debt buyers and collections agencies places more power in the hands of the collectors and leaves companies with less ability to choose good actors.

It's a prime example of where regulations can help.

Much needed regulatory protections

A knee-jerk reaction may be to do away with third-party debt collectors entirely. But we can't.

A key role of financial services is to facilitate the movement of money from those who have it to those that need it. If that money is being extended as a loan, there has to be an expectation that it will be paid back. When money isn't consistently paid back, less money is lent in the future. That means young families can't get mortgages, the soon-to-open corner pizza joint can't get a loan to start the business, and the system as a whole grinds to a halt. Debt collections help guarantee lenders that debts will be repaid.

A 2017 paper published by the NY Federal Reserve made the point apparent:

Our analysis suggests that restricting collection activities leads to a decrease in access to credit and to a deterioration in indicators of financial health... We find a sizable and significant reduction in auto loan balances, a significant decline in credit card and non-traditional finance balances, a significant decrease in auto and credit card originations, a sizable and significant increase in delinquent credit card balances and non-traditional finance balances, and a small but statistically significant reduction in credit scores.

Regulations create a more level playing field that balances the needs of the lender to get paid back with the rights of the borrower not to be abused.

This is different than what I advocated for with overdraft fees. With overdrafts, banks are competing for new customers by offering them a new service that the customers value. Regulations play an important role requiring that banks inform customers of the details, but if the customer doesn't like the service they can take their business elsewhere.

With debt collections, the debtor doesn't get a choice of debt collector. Competition doesn't work as a feedback mechanism to rein in potential abuse. Regulations have to play that role instead.

At the federal level, the primary regulation is the Fair Debt Collection Practices Act (FDCPA) passed in 1977 and as subsequently amended. The Consumer Financial Protection Bureau (CFPB) is responsible for rule-making. The CFPB and Federal Trade Commission (FTC) are jointly responsible for enforcement.

The FDCPA has two basic elements - what you have to do as a debt collector and what you can't do. For example - you have to bring legal action against consumers in the district where the contract was signed or the consumer lives and you cannot call a consumer about a particular debt more than seven times in seven days. The full rule, with new amendments effective November 2021, runs about 100 pages. The recent amendments helped bring the FDCPA into the twenty-first century with clarification around text messages (okay), email (okay but not to work email addresses), and social media (okay as long as private).

Like many financial regulations in the US, those governing debt collections are a bit of a mess. Each state also has its own regulations governing debt collection. State-level legislation mostly governs state-specific surety bonds and licensing, penalties, and statutes of limitation. There's significant variance state to state. Thirty-two states require licenses to operate, twenty-nine states require surety bonds, penalties range from $1000 to $10,000 per violation, and the period of time when collectors can file lawsuits varies from three to fifteen years.

This morass of highly detailed and overlapping regulatory regimes is a meaningful barrier to entry. TrueAccord, a well-funded startup founded in 2013, took over two years to become fully licensed in all 50 states.

Despite the real costs to new entrants and the resulting impacts on competition, it appears that the regulations are doing a reasonable job. While the collections industry generates a tremendous volume of complaints, only 0.09% of the 170,000+ complaints to the Consumer Financial Protection Bureau resulted in an investigation. Debt buyers generated investigations at 25 times the rate of agencies. It seems competition among agencies - driven by the companies that hire them for long-term relationships - is a strong antidote to abusive practices.

Nonetheless, while many debt collection practices may fall beneath the threshold of "consumer abuse," there's clearly significant room for improvement.

Debt Collectors Old & New

Holes in the regulations are not hard to find. Take the "seven calls in seven days" restriction mentioned earlier. That's specific to a particular debt. What if you have multiple delinquent debts in collections?

Daily contact attempt limits ranged from three calls to as many as 15 per account... No issuer allowed calls to continue within a given day once “right party contact” has been made. Right party contact occurs when the issuer or collector is able to reach and speak with the consumer the issuer believes is responsible for the debt via telephone. Right party contact rates typically fell between 3% and 7% for in-house and first-party collections and between 0.5% and 2.0% for third-party collections over a three month period.

The daily limits are self-imposed. If we extrapolate from the 0.5% right party contact success rate, we find that third-party debt collectors make an average of two hundred calls to a consumer before they get ahold of them. At the fifteen call-per-day limit, that's two hundred calls in two weeks. From a regulatory standpoint, not abuse, but clearly could be improved upon. Such practices help explain why collections rates are so low.

Legacy body shops

Many of the legacy debt collections agencies embody the worst of body shops, a less-than-polite term for companies that employ huge numbers of employees in mid-skill, labor-intensive short to midterm contract-based services. Historically, the primary differentiators among body shops were their abilities to train new employees quickly and cut costs. Cutting costs inevitably gave rise to relocating or rehiring employees in lower-cost countries. More recently, these same companies have employed software automation, such as robocalls, to bring costs down further.

Expert Global Solutions, a company since acquired by Alorica in 2016, was a poster child for these types of businesses. At the time it was the largest debt collector in the world and employed 32,000 people in 100 locations across 10+ countries. It generated over $1 billion in revenue per year. It was fined for FDCPA violations in 2013 on charges of:

using tactics such as calling consumers multiple times per day, calling even after being asked to stop, calling early in the morning or late at night, calling consumers’ workplaces despite knowing that the employers prohibited such calls, and leaving phone messages that disclosed the debtor’s name, and the existence of the debt, to third parties... [T]he companies also continued collection efforts without verifying the debt, even after consumers said they did not owe it.

In its mere four years of existence, the company also accounted for 1821 complaints to the CFPB.

That's not to say all debt collection agencies are bad. Summit Account Resolution, founded in 1996, makes a point not to use robocallers and focus on "preserving human dignity." They've successfully helped 12,700 consumers out of debt delinquency this past year and recovered over $140 million since its founding. The success didn't come at the cost of abusing consumers - recovery rates are twice the industry average, complaints are just a fraction, and the company is Better Business Bureau accredited with a perfect A+ rating.

The challenge is that a business with a model like Summit's doesn't scale well. It's difficult and expensive to hire and retain the high-quality employees necessary to provide such a service. And yet, Summit's success demonstrates that if you treat people better, it can be good business.

That's an insight that hasn't been lost on fintech startups.

Startup digital debt collectors

Technology can allow a company to provide a higher quality of service - treating people like people - without the cost burden of a large employee base. Done right, it can be revolutionary for debt collection.

Startups offer two different solutions to the industry - a digital collections agency or digital collections technology. A digital collections agency improves on the traditional agency model by (1) using technology to enable self-service delinquent debt resolutions and (2) enabling the agency employees to consistently provide a better, more personalized experience for every consumer. Digital collections technology offers the same services but to the employees of other collectors or in-house teams.

TrueAccord is one of the oldest and most well-funded startups in debt collections. Founded in 2013, they started as a digital collections agency with services in all 50 states. They've since raised $47 million in venture capital funding and expanded the business to also sell a white-labeled version of the technology to in-house teams. If a business managing delinquent consumer debt wants to collect the debt in-house or work with a third-party agency, TrueAccord has a product that can help.

There are three key elements to the technology:

Meet customers where they want to be met,

Optimize each interaction to meet that customer's wants and needs, and

Use machine learning to measure 1 and 2 to make continual improvements.

As a digital-first agency, TrueAccord truly embraces a multichannel approach. They'll engage customers through email, text messages, and private social media messages. All of these channels are fundamentally different than phone calls - they're asynchronous. A phone call requires the collector and consumer to engage at the same time, reducing the probability that the two meet and likely disrupting the consumer's day if they do. Asynchronous communications allow the collector to notify the consumer and the consumer to respond at their leisure.

Each interaction can then be customized to create a unique consumer journey. Messages can be timed so that they meet the customer's schedule. Message content can be configured so that it resonates, whether that's by changing the tone or the voice. Payment schedules can be modified so the consumer can get their debts back on track. It's a win-win - the consumer is happier and TrueAccord collects more of the delinquent debts.

Underpinning the whole debt collections platform is machine learning. TrueAccord has worked with over 24 million consumers. Every email click, every message opened creates data that can be used to make the experience just a little bit better for the next consumer. The compounding effect is remarkable.

The success shows up in the numbers. The startup has collection rates 50-80% higher than the industry averages. 96% of consumers self-service their debts without ever talking to a person. It's a more successful and lower cost than traditional models. That's probably why companies like Shopify, WePay, and oDesk all count themselves as TrueAccord customers.

The success doesn't come at the cost of a better customer experience, quite the opposite. The BBB accredited startup maintains an almost-perfect A rating. The company has a Net Promoter Score of 40, way better than the average score of 30 for banks. The customer reviews are glowing, of a quality that any company would be proud to flaunt.

It's a remarkable success story in an industry that sorely needs change. But success like that doesn't go unnoticed.

InDebted started a few years after TrueAccord in 2016. The company used the heterogeneous global regulatory environment to its advantage, a common and highly successful playbook in financial services. They launched as a digital collections agency model similar to TrueAccord but did so in Australia where the regulations and licensing are materially different. The company has since raised $41 million and expanded into New Zealand, Canada, and just recently the US. US expansion was achieved via acquisition - it's often cheaper and faster to purchase a company that already has the required licensing than it is to build it yourself.

Other startups have taken a different tack and attempted to compete by just selling digital collections technology without any agency offering. Symend launched out of Canada in 2016 and markets that over 100 million end-consumers have used the product. That's a tremendous amount of data to feed the machine learning-based platform. It's a data-intensive technology business, meaning it avoids much of the regulatory overhead and liability of actually operating an agency. It's a particularly good fit for venture capitalists, likely a reason why the company has successfully raised over $100M since its founding.

Prodigal and Receeve are quickly following in the footsteps of Symend. Founded in 2018 and 2019, respectively, they've each raised significant funding from venture capital for tech-only offerings. Where Prodigal is US-focused, Receeve is tackling Europe. In a come full circle story, Prodigal counts TrueAccord as one of their clients.

The Future of Debt Collections

Debt collections aren't just here to stay, they'll continue to grow. As the consumer population grows and consumers take on ever more debt, the need for collections will never be greater.

We're already starting to see consumers take on new and different types of debt than they have historically. Buy Now Pay Later is just one example, those now-ubiquitous buttons you see during online checkout where you can choose to "pay in four installments" rather than pay the full cost today. If looked at your upcoming credit card statement recently, you've likely seen similar offers for purchases you already made. It's part of a future predicted by venture capitalist Andreessen Horowitz and others where "every company will be a fintech company."

There's work to be done to help consumers avoid taking on so much debt that they fall into delinquency in the first place, but that's a topic for a different letter. The fact remains that for those consumers that do, the collections experience today is almost universally poor.

Startups are meaningfully changing the dialogue for the first time. Summit Account Resolution proved that you can generate much higher collections rates if you help people in delinquency rather than abuse them, but the company can only serve a couple thousand people a year. That won't be meaningful for the 77 million consumers with debt today.

Startups are using technology to scale that insight to millions, creating better experiences for consumers and higher recovery rates for businesses. In the vast majority of cases, debt delinquency isn't because someone doesn't want to pay. It's because they can't. Consumers deserve to be treated with respect and given the help they need to get their finances back on track. While financial advisors and investing platforms find themselves in the limelight, debt collections startups are doing equally meaningful work for millions of consumers well away from the headlines.

Debt collection is a critically important part of our economy. It's an industry that's just beginning to see meaningful change and I have no doubt there is much more to come.

Cocktail Talk

PayPal is exploring launching a stablecoin. Stablecoins are digital representations of fiat currency, like the dollar, that can be exchanged for a dollar with the issuer. Such instruments benefit from the safety and soundness guarantees provided to the banking industry, but PayPal isn't a bank. I explained why and predicted how they'll launch the stablecoin. (Twitter)

Overdraft fees are going the way of the dinosaur. I predicted the end of overdrafts in a previous letter - competition for new customers is too great to let a now high-profile service like overdrafts be a barrier. Bank of America is now the latest in this race to compete for customers by eliminating overdraft fees. (Bank of America)

JP Morgan successfully tested their new digital currency system with the Central Bank of Bahrain. Using JPM Coin, Bank ABC and client Aluminium Bahrain were able to exchange dollar-based payments without any intermediary. It's another major milestone in the slow revolution to reinvent money movement. Such disintermediation may lead to as much as $100 billion in reduced cross-border payment costs. (Ledger Insights)

Scientists discovered over 60 million active fish nests deep beneath the Antarctic. The nests are like you'd expect for birds, just with fish. The discovery dwarfs the next largest known assemblage of nesting fish which measures in the hundreds. It's an exciting example of just how amazing our world is. If millions of nesting fish can hide in plain sight, what else is there to discover? (ScienceNews)

Your Weekly Cocktail

I'm still on a Negroni kick! This one exemplifies just how versatile the drink can be.

Toffee Negroni

1.0oz Bully Boy The Rum Cooperative Vol. 2

1.0oz Amontillado Sherry

1.0oz Aperol

Orange peel

Pour all of the ingredients into a mixing glass. Add ice until it comes up over the liquid. Stir for ~20 seconds until the glass is frosted, ~50 times. Add ice to a rocks glass. Strain the drink into the rocks glass. Squeeze the orange peel over the drink to express the oils and drop in.

I love cocktails that take a well-known recipe, keep the spirit, and still blow the original out of the water. This one, courtesy of Difford's Guide, does exactly that. The traditional Negroni featured last week is gin, sweet vermouth, and the bitter-sweet amaro Campari in equal proportions. This starts with the same basics - equal proportions of a high proof spirit, a fortified wine, and an amaro - but we end up with a totally different drink. It's exactly as the name implies, a sweet toffee flavor reined in by the bitterness of the amaro. It's a wild combination that I've enjoyed in front of a fire, with dinner, and after dinner. The cocktail's great and the versatility is awesome. Ten out of ten would recommend.

Cheers,

Jared